Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

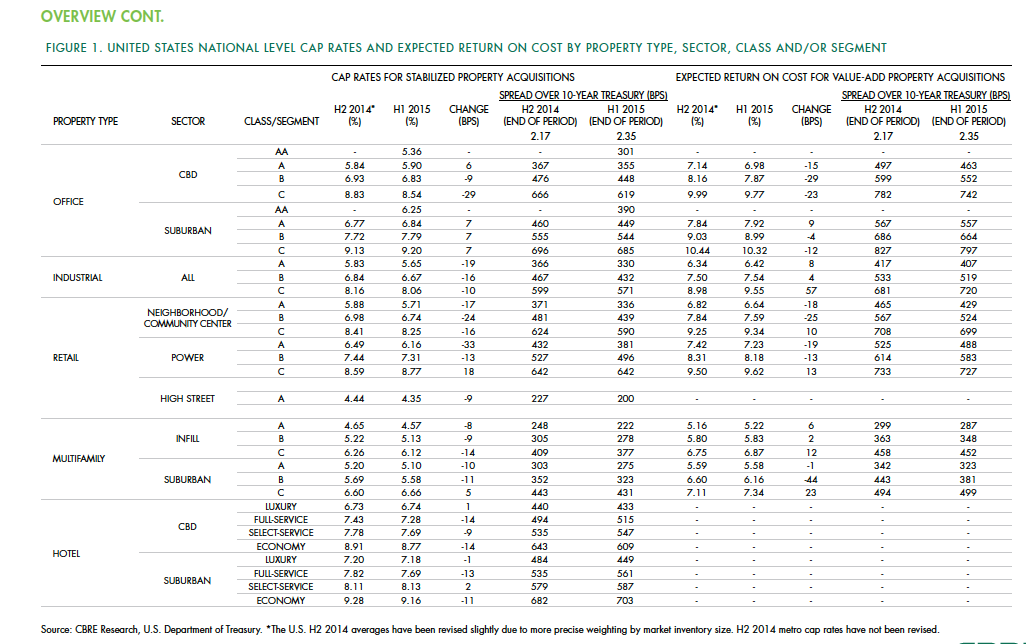

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

| Aug 20, 2013

Code amendment in Dallas would limit building exterior reflectivity

The Dallas City Council is expected to vote soon on a proposed code amendment that would limit a building’s exterior reflectivity of “visible light” to 15%.

| Aug 16, 2013

Today's workplace design: Is there room for the introvert?

Increasingly, roaming social networks are praised and hierarchical organizations disparaged, as workplaces mimic the freewheeling vibe of the Internet. Research by Susan Cain indicates that the "openness" pendulum may have swung too far.

| Aug 14, 2013

Green Building Report [2013 Giants 300 Report]

Building Design+Construction's rankings of the nation's largest green design and construction firms.

| Aug 13, 2013

DPR's Phoenix office, designed by SmithGroupJJR, affirmed as world's largest ILFI-certified net-zero facility

The new Phoenix Regional Office of DPR Construction, designed by SmithGroupJJR, has been officially certified as a Net Zero Energy Building by the International Living Future Institute (ILFI). It’s the largest building in the world to achieve Net Zero Energy Building Certification through the Institute to date.

| Aug 8, 2013

Stanley Hardware introduces Flexi-Felt for protecting floors

Stanley Hardware offers a solution to the frustrating problem of protecting your floors. The answer is Flexi-Felt®, an innovative product line that eliminates the aggravation of frequently replacing felt pads and leg tips that usually wear down or fall off, causing damage to expensive floors.

| Aug 8, 2013

New green property index could boost REIT investment in more sustainable properties

A project by the National Association of Real Estate Investment Trusts (NAREIT), the FTSE Group, and the U.S. Green Building Council to jointly develop a Green Property Index could help REITs attract some of the growing pool of socially responsible investment money slated for green investments.

| Aug 6, 2013

CoreNet: Office space per worker shrinks to 150 sf

The average amount of space per office worker globally has dropped to 150 square feet or less, from 225 square feet in 2010, according to a recent global survey conducted by CoreNet Global.

| Aug 6, 2013

Australia’s first net zero office building features distinctive pixelated façade

Australia's first carbon neutral office building, featuring a distinctive pixelated façade, recently opened in Melbourne.

| Jul 30, 2013

In support of workplace chatter

As the designers of collaborative work environments, architects and engineers understand how open, transparent spaces can cultivate the casual interaction and knowledge sharing that sparks innovation. Now a new study reveals another potential benefit of open workplaces: social interaction that supports happier employees.

| Jul 29, 2013

2013 Giants 300 Report

The editors of Building Design+Construction magazine present the findings of the annual Giants 300 Report, which ranks the leading firms in the AEC industry.