Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

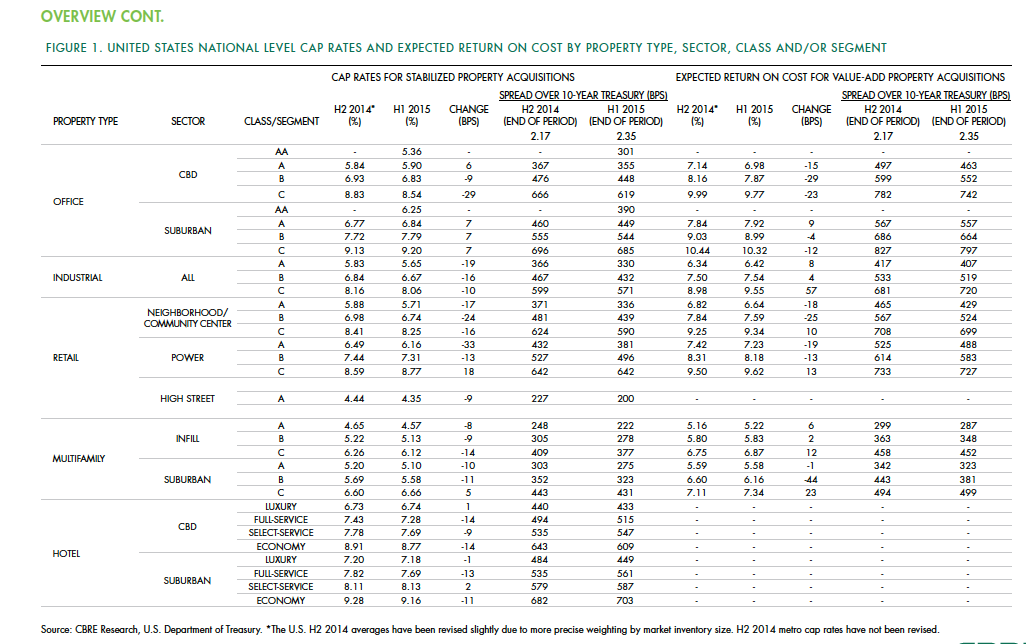

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Office Buildings | Feb 15, 2019

A healthier perspective: Office developers bet on wellness amenities to attract top-notch tenants

Owners and developers are driving demand for wellness features and practices—active stairways, biophilia, enhanced air quality, etc.—as one more way draw tenants.

Office Buildings | Feb 15, 2019

Vancouver’s new office building will be a stack of reflective boxes

OSO and Merrick Architecture designed the building.

Office Buildings | Feb 11, 2019

Real-world wellness pays off

3form, a materials manufacturer, did a top-to-bottom remodel of its Salt Lake City headquarters campus that included adding a 14,500-sf gym.

Office Buildings | Feb 5, 2019

Duluth Trading Company moves to new HQ building

Plunkett Raysich Architects designed the project.

Interior Architecture | Jan 14, 2019

To get more involved earlier in projects, a leading furniture dealer launches a firm for commercial interiors construction

Vantis is positioned to integrate design with offsite customized fabrication.

Office Buildings | Jan 11, 2019

Open offices are bad!

The Harvard studies on the unintended effects of open office defines it as space where 'one entire floor was open, transparent and boundaryless… [with] assigned seats,' and the other had 'similarly assigned seats in an open office design, with large rooms of desks and monitors and no dividers between people's desks.'

Office Buildings | Dec 18, 2018

Google announces new $1B Hudson Square campus project

The 1.7 million-sf campus will expand the company’s New York City presence.

Office Buildings | Dec 13, 2018

Apple selects Austin for $1 billion campus

The company will also build smaller expansions in six other U.S. cities over the next three years.

Office Buildings | Dec 4, 2018

Brookfield launches contest for startups to receive two years of free office space

This is part of a larger campaign to burnish the image of L.A.’s Wells Fargo Center.

Office Buildings | Nov 28, 2018

Amazon HQ2 and the new geography of work

The big HQ2 takeaway is how geography and mobility are becoming major workplace drivers.