Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

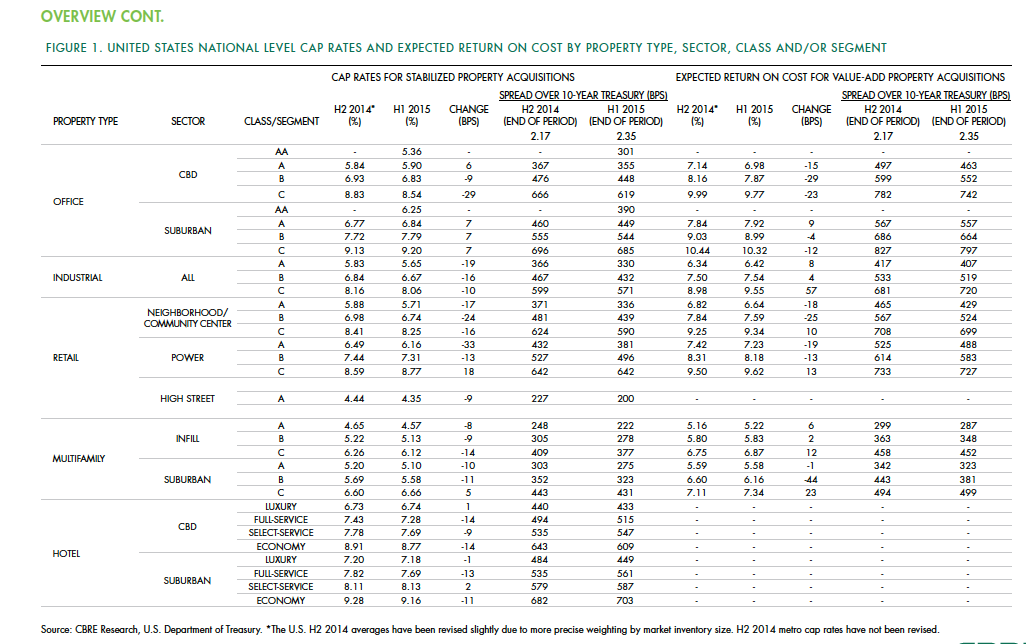

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

| Apr 6, 2012

Flat tower green building concept the un-skycraper

A team of French designers unveil the “Flat Tower” design, a second place winner in the 2011 eVolo skyscraper competition.

| Apr 2, 2012

EB-5 investment funds new Miramar, Fla. business complex

Riviera Point Holdings breaks ground on $17 million office center.

| Mar 28, 2012

Milestone reached for LEED-certified buildings?

Total number of major global green buildings now stands at 12,000.

| Mar 27, 2012

Bank of America Plaza becomes Atlanta's priciest repo

Repo will help reset market prices for real estate, and the eventual new owner will likely set rental rates at a new or near the bottom and improve the facilities to lure tenants.

| Mar 26, 2012

McCarthy tops off Math and Science Building at San Diego Mesa College

Designed by Architects | Delawie Wilkes Rodrigues Barker, the new San Diego Mesa College Math and Science Building will provide new educational space for students pursuing degree and certificate programs in biology, chemistry, physical sciences and mathematics.

| Mar 26, 2012

Ball State University completes nation's largest ground-source geothermal system

Ball State's geothermal system will replace four aging coal-fired boilers to provide renewable power that will heat and cool 47 university buildings, representing 5.5-million-sf on the 660-acre campus.

| Mar 21, 2012

10 common data center surprises

Technologies and best practices provide path for better preparation.

| Mar 20, 2012

New office designs at San Diego’s Sunroad Corporate Center

Traditional office space being transformed into a modern work environment, complete with private offices, high-tech conference rooms, a break room, and an art gallery, as well as standard facilities and amenities.

| Mar 16, 2012

Temporary fix to CityCenter's Harmon would cost $2 million, contractor says

By contrast, CityCenter half-owner and developer MGM Resorts International determined last year that the Harmon would collapse in a strong quake and can't be fixed in an economical way. It favors implosion at a cost of $30 million.