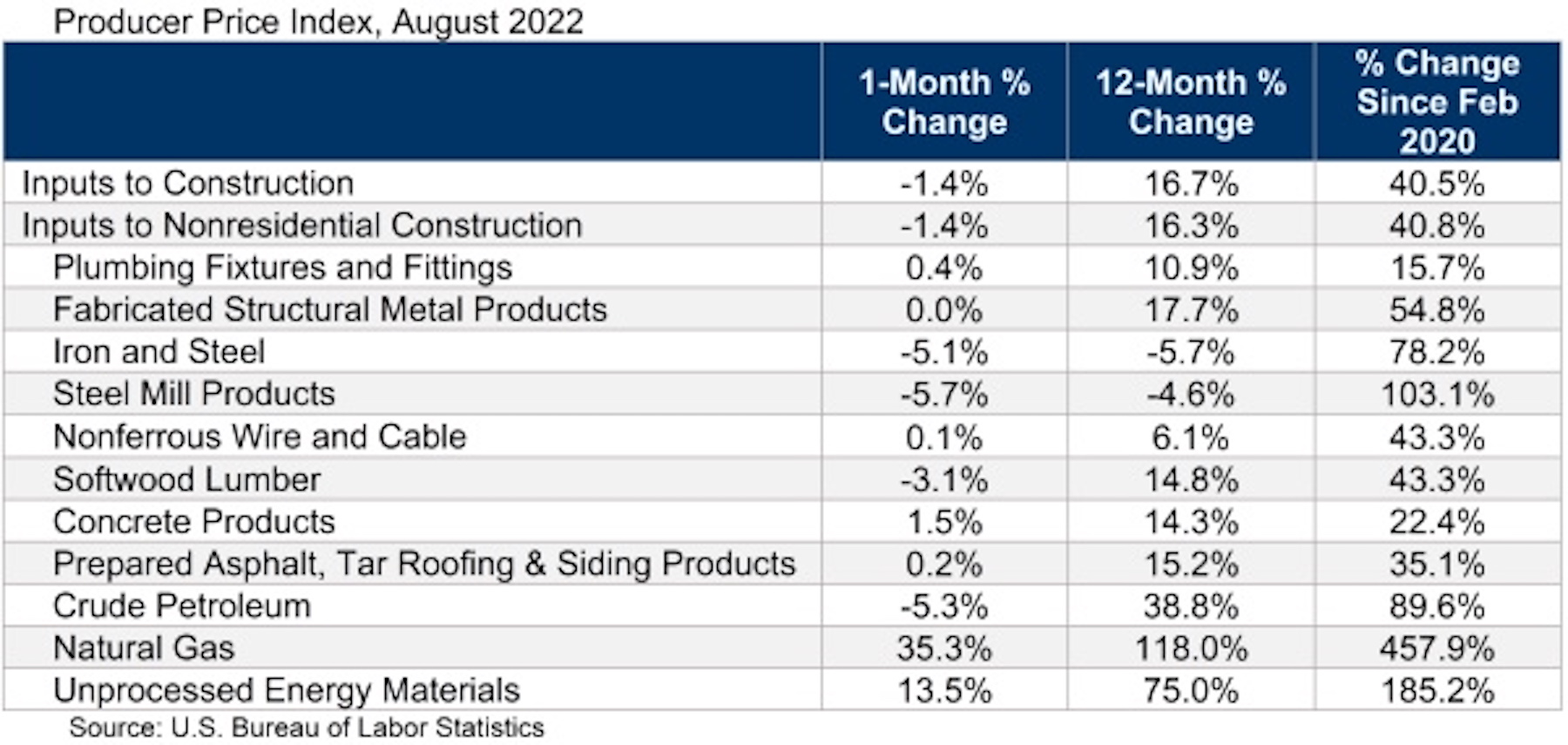

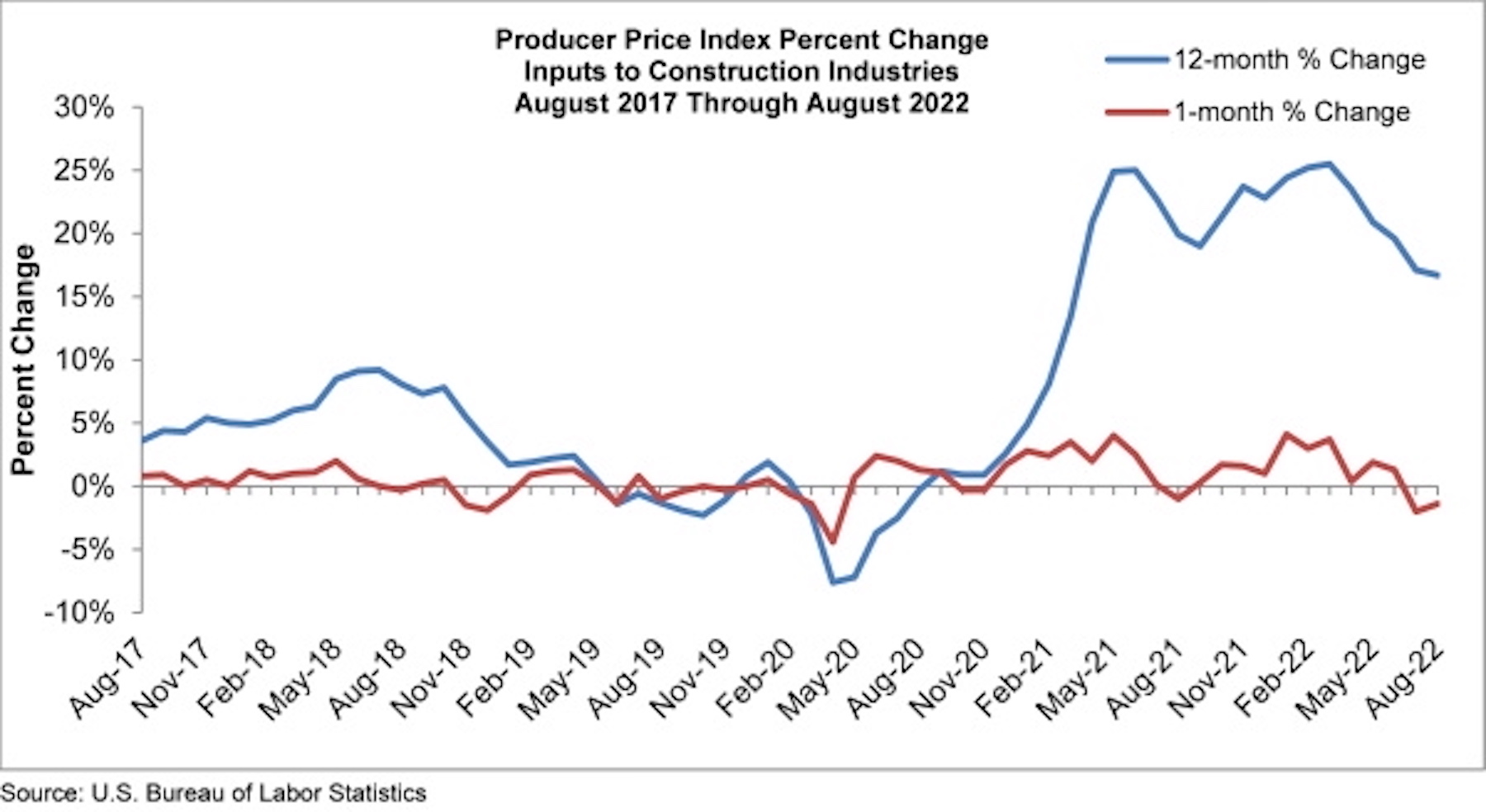

Construction input prices decreased 1.4% in August compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices fell 1.4% for the month as well.

Construction input prices are up 16.7% from a year ago, while nonresidential construction input prices are 16.3% higher. Input prices were up in six of 11 subcategories* on a monthly basis. Natural gas prices increased 35.3% (and are 457.9% higher than they were in February 2020), followed by unprocessed energy materials prices, which rose 13.5%. Crude petroleum prices were down 5.3% in August.

"Until yesterday's Consumer Price Index report, investors and other market-watchers had been delighted by recent inflation news," said ABC Chief Economist Anirban Basu. "Today's Producer Price Index report supplies additional evidence that wholesale inflation is edging lower from the highs observed earlier this year. While this may create a sense of relief among contractors, this is no time for complacency.

"With COVID-19 lockdowns persisting in China, the world's leading manufacturer, and Europe facing severe energy crises, supply chain disruptions will persist," said Basu. "That suggests that construction materials and equipment prices are likely to remain elevated even if year-over-year price increases moderate. Public construction workers remain in short supply, including in the category of public construction. The upshot is that inflation is poised to remain stubbornly high even as some begin to declare victory. Estimators and others in the construction industry should be on guard for occasional surges in inflation during the months ahead."

Based on ABC's Construction Confidence Index and Backlog Indicator, many contractors expect to pass along their cost increases to project owners during the months ahead," said Basu. "Some contractors may be in for a rude surprise. With borrowing costs rising and risk of recession elevated, it is perfectly conceivable that project owners will become increasingly resistant to elevated charges for the delivery of construction services. Based on nonresidential construction spending data, that process has already begun. Accordingly, contractors should remain laser-focused on cashflow and weeding out costs as opportunities arise."

Related Stories

Giants 400 | Oct 30, 2023

Top 170 K-12 School Architecture Firms for 2023

PBK Architects, Huckabee, DLR Group, VLK Architects, and Stantec top BD+C's ranking of the nation's largest K-12 school building architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Oct 30, 2023

Top 100 K-12 School Construction Firms for 2023

CORE Construction, Gilbane, Balfour Beatty, Skanska USA, and Adolfson & Peterson top BD+C's ranking of the nation's largest K-12 school building contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Oct 30, 2023

Top 80 K-12 School Engineering Firms for 2023

AECOM, CMTA, Jacobs, WSP, and IMEG head BD+C's ranking of the nation's largest K-12 school building engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report.

MFPRO+ Special Reports | Oct 27, 2023

Download the 2023 Multifamily Annual Report

Welcome to Building Design+Construction and Multifamily Pro+’s first Multifamily Annual Report. This 76-page special report is our first-ever “state of the state” update on the $110 billion multifamily housing construction sector.

Giants 400 | Oct 23, 2023

Top 115 Multifamily Construction Firms for 2023

Clark Group, Suffolk Construction, Summit Contracting Group, Whiting-Turner Contracting, and McShane Companies top the ranking of the nation's largest multifamily housing sector contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking factors revenue for all multifamily buildings work, including apartments, condominiums, student housing facilities, and senior living facilities.

Senior Living Design | Oct 19, 2023

Senior living construction poised for steady recovery

Senior housing demand, as measured by the change in occupied units, continued to outpace new supply in the third quarter, according to NIC MAP Vision. It was the ninth consecutive quarter of growth with a net absorption gain. On the supply side, construction starts continued to be limited compared with pre-pandemic levels.

Warehouses | Oct 19, 2023

JLL report outlines 'tremendous potential' for multi-story warehouses

A new category of buildings, multi-story warehouses, is beginning to take hold in the U.S. and their potential is strong. A handful of such facilities, also called “urban logistics buildings” have been built over the past five years, notes a new report by JLL.

Building Materials | Oct 19, 2023

New white papers offer best choices in drywall, flooring, and insulation for embodied carbon and health impacts

“Embodied Carbon and Material Health in Insulation” and “Embodied Carbon and Material Health in Gypsum Drywall and Flooring,” by architecture and design firm Perkins&Will in partnership with the Healthy Building Network, advise on how to select the best low-carbon products with the least impact on human health.

Contractors | Oct 19, 2023

Crane Index indicates slowing private-sector construction

Private-sector construction in major North American cities is slowing, according to the latest RLB Crane Index. The number of tower cranes in use declined 10% since the first quarter of 2023. The index, compiled by consulting firm Rider Levett Bucknall (RLB), found that only two of 14 cities—Boston and Toronto—saw increased crane counts.

Office Buildings | Oct 19, 2023

Proportion of workforce based at home drops to lowest level since pandemic began

The proportion of the U.S. workforce working remotely has dropped considerably since the start of the Covid 19 pandemic, but office vacancy rates continue to rise. Fewer than 26% of households have someone who worked remotely at least one day a week, down sharply from 39% in early 2021, according to the latest Census Bureau Household Pulse Surveys.