Industrial development continues to be a growth sector for many metros, especially in the western U.S. But aggressive building may be finally catching up with that sector’s demand, at least temporarily.

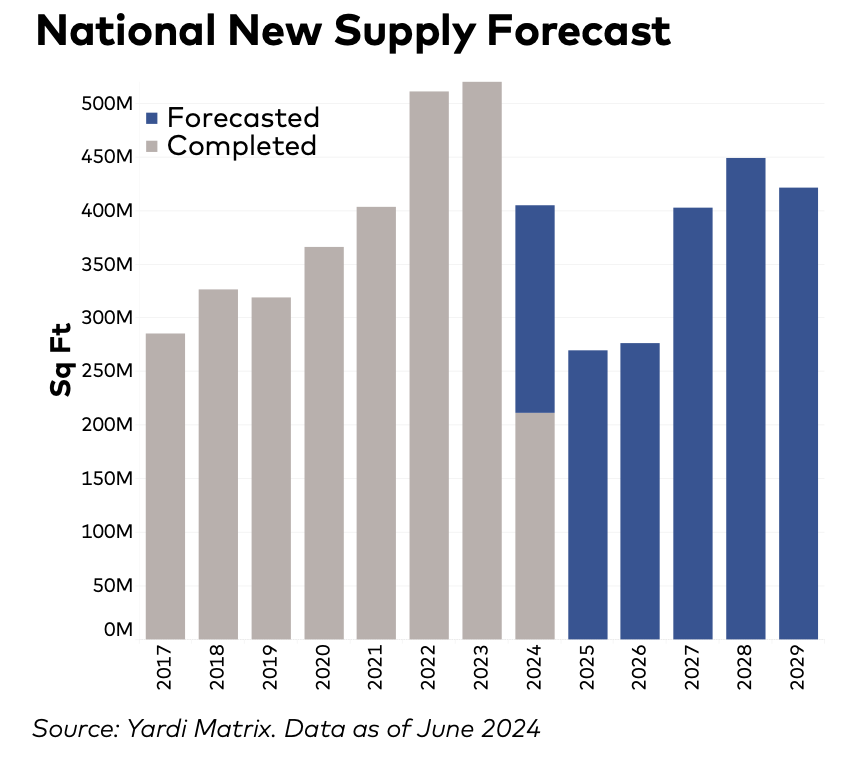

After two years of record-smashing deliveries, the industrial pipeline has slowed in a number of markets. In its latest National Industrial Report, CommercialEdge estimates that 97.8 million sf of industrial space were started in the first half of 2024, a 33% decline from the same period a year earlier. By comparison, 1.1 billion sf were started between 2021 and 2022, with 313 million sf started in the first half of 2022 alone. The latest slowdown in starts has been occurring for the past six quarters, says CommercialEdge, which attributes the erosion to “normalized” tenant demand, oversupply, rising construction costs, and “economic uncertainty.”

Nationwide, 375.7 million sf of industrial space were in various stages of construction through the first half of 2024, representing 1.9% of total stock. In the latest six-month period, 209 million sf of new space were delivered, compared to 160 million sf in the first half of 2022. “This growth underscores the market’s capacity to bring projects to completion despite the decline in construction starts,” CommercialEdge states.

This sector has gotten a big bump from manufacturing, which accounted for 16.1% of annualized industrial construction starts through June, compared to an estimated 7.5% in 2018 through 2021, and more than 13% in 2022 and 2023. As more manufacturing returns to the U.S., demand for industrial space is expected to benefit.

Indeed, CommercialEdge forecasts that the new development pipeline will grow in the next few years, but at a slower clip. It points out that developers have disclosed plans for 561.2 million sf of new space. “Once the market absorbs the recently completed stock, and the cost of capital begins to decrease, we expect many of these projects to see shovels in the ground,” predicts CommercialEdge.

Vacancy rates and rents for industrial space rising

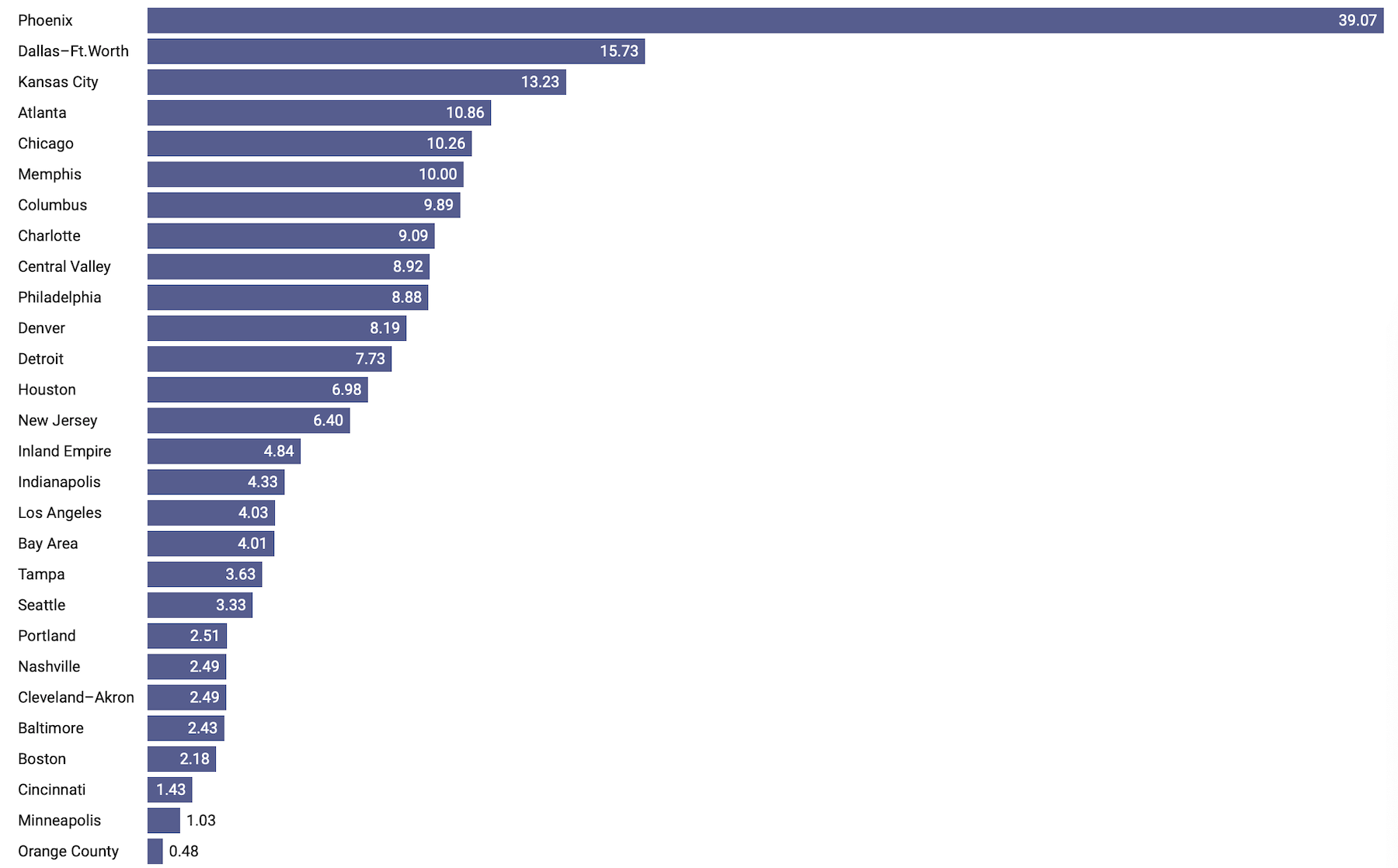

Phoenix leads the country by far in industrial space under construction, with 39.07 million sf under construction. The next-closest metro was Dallas-Fort Worth, at 15.23 million sf. DFW’s vacancy rate sat at a relatively manageable 6.5%, but it appears this market is “hitting the brakes” on new development after delivering 126.4 million sf of industrial space since the start of 2022.

Nationally, the vacancy rate for industrial space stood at 6.1%, up slightly. The national average rent in June was $8.04 per sf, although the average for contracts signed over the previous 12 months was $10.56. The San Francisco Bay Area recorded the highest average rent, at $13.34, and $16.24 per sf for newer contracts. Miami experienced the largest premium for new leases that, at $17.35, cost tenants $5.85 more than the national average.

California’s Inland Empire led the nation in rent growth, with in-place rents rising 12.5% year-over-year. Conversely, the Midwest saw the slowest rent growth: In Kansas City, for example, in-place rents increased only 2.5%; in St. Louis, 3.4%.

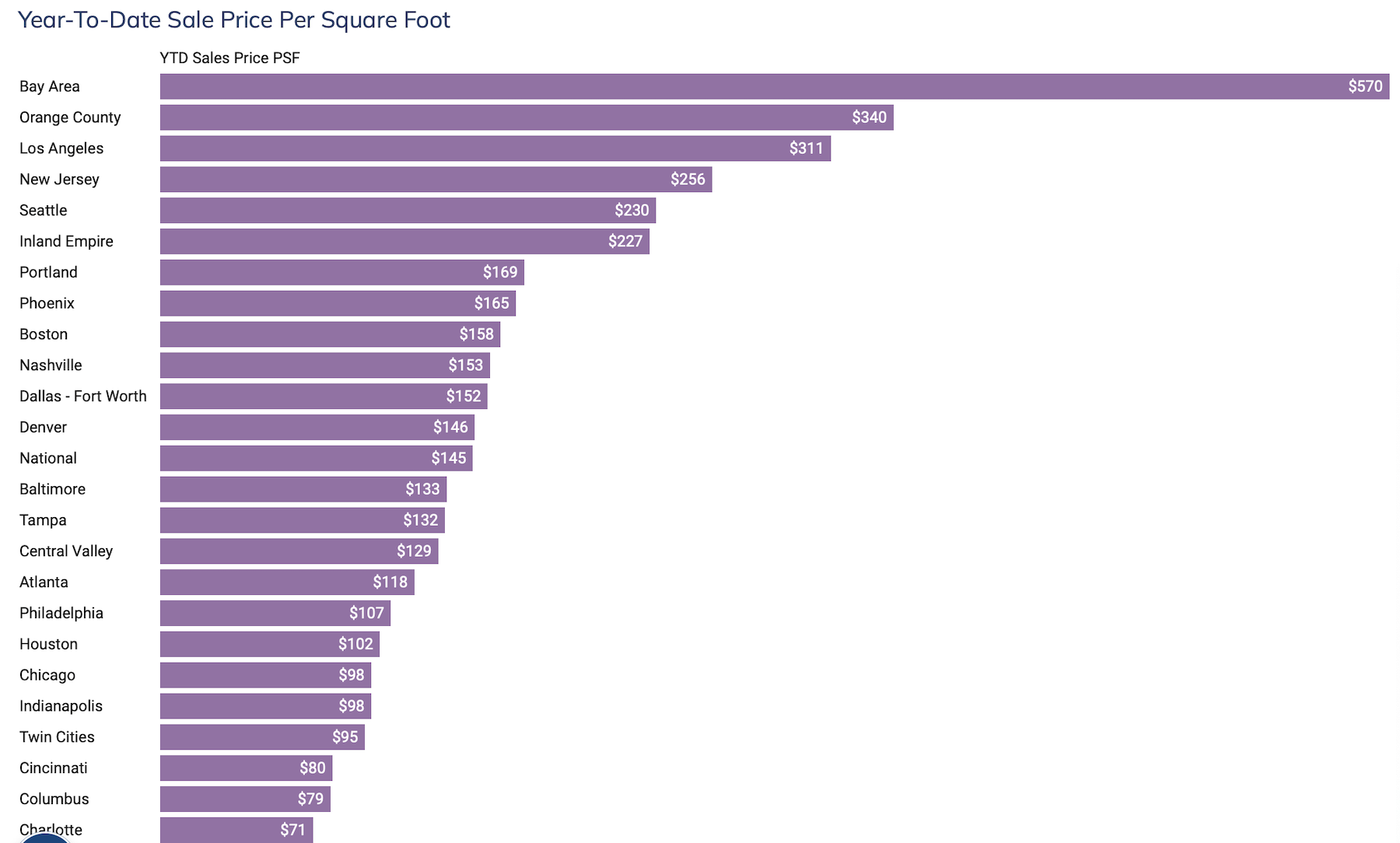

Bay Area leads industrial sales

The sale of industrial buildings totaled $25.1 billion through the first half of 2024, and demand remains strong, with the average sale price of $139 per sf rising 12.9% over the same period in 2023, according to CommercialEdge estimates.

Again, the Bay Area led all markets in year-to-date industrial sales, at $2.285 billion. San Francisco was followed by Dallas-Fort Worth ($2.006 billion), Los Angeles ($1.581 billion, and Chicago ($1.314 billion).

Southern California remains the most sought-after location for distribution center and warehouse sales and development. CommercialEdge notes that earlier this year Rexford Industrial Realty paid $1 billion for 3 million sf across 48 properties in L.A. and Orange counties.

The Bay Area led the nation in average sales price per sf, at $570. This market has seen a spike in demand for advanced manufacturing space. Over 4 million sf of industrial space are under construction in the Bay Area.

In the South, the surge in Texas’s population—it’s the fastest-growing state in the U.S.—drove demand for industrial space, with DFW serving as a hub from products arriving from Mexico, which recently surpassed Canada as America’s largest trading partner, according to the Census Bureau. That positioning is why CommercialEdge expects Dallas-Fort Worth’s industrial development and construction to eventually pick up steam again.

Other markets worth keeping an eye on include Charlotte and Nashville, with their low vacancy rates and tight supply.

On the other hand, Boston—one of the country’s most expensive markets—reported the highest industrial vacancy rate, at 8.8%. New Jersey, another pricy rent market, nevertheless remained a regional leader in industrial sales, with over $1 billion in transactions closing through June.

Related Stories

| Oct 1, 2014

4 trends shaping the future of data centers

As a designer of mission critical facilities, I’ve learned that it’s really difficult to build data centers to keep pace with technology, yet that’s a reality we face along with our clients, writes Gensler's Jackson Metcalf.

| Sep 24, 2014

Architecture billings see continued strength, led by institutional sector

On the heels of recording its strongest pace of growth since 2007, there continues to be an increasing level of demand for design services signaled in the latest Architecture Billings Index.

| Sep 22, 2014

4 keys to effective post-occupancy evaluations

Perkins+Will's Janice Barnes covers the four steps that designers should take to create POEs that provide design direction and measure design effectiveness.

| Sep 22, 2014

Sound selections: 12 great choices for ceilings and acoustical walls

From metal mesh panels to concealed-suspension ceilings, here's our roundup of the latest acoustical ceiling and wall products.

| Sep 19, 2014

Smithsonian Institution opens LEED Platinum lab facility

The Charles McC. Mathias Laboratory will emit 37% less CO2 than a comparable lab that does not meet LEED-certification standards.

| Sep 17, 2014

New developments in data center design

From the dozen or so facilities housing Google’s 900,000 servers to the sprawling server farms of Facebook to Amazon’s seven sites scattered around the world, today’s data centers must accommodate massive power demand, high heat loads, strict maintenance protocols, and super-tight security. This AIA Discovery course is worth 1.0 AIA CES HSW learning units.

| Sep 9, 2014

Using Facebook to transform workplace design

As part of our ongoing studies of how building design influences human behavior in today’s social media-driven world, HOK’s workplace strategists had an idea: Leverage the power of social media to collect data about how people feel about their workplaces and the type of spaces they need to succeed.

| Sep 7, 2014

Ranked: Top state government sector AEC firms [2014 Giants 300 Report]

PCL Construction, Stantec, and AECOM head BD+C's rankings of the nation's largest state government design and construction firms, as reported in the 2014 Giants 300 Report.

| Sep 3, 2014

New designation launched to streamline LEED review process

The LEED Proven Provider designation is designed to minimize the need for additional work during the project review process.

| Sep 2, 2014

Ranked: Top green building sector AEC firms [2014 Giants 300 Report]

AECOM, Gensler, and Turner top BD+C's rankings of the nation's largest green design and construction firms.