The deterioration in construction output growth across emerging markets has been worse than previously expected, particularly in the US and the Middle East. Therefore, the forecast for global construction output growth in 2019 has been revised down to 2.7%, which will be the slowest pace of growth in a decade, according to GlobalData, a leading data and analytics company.

GlobalData’s central forecast sees global construction output growth increase to 3.2% in 2020 and then stabilize at 3.4% over the remainder of the forecast period, which runs to 2023. According to the company’s latest report, ‘Global Construction Outlook to 2023 – Q3 2019 Update’, this is partly driven by a projected improvement in the global economy in 2020, which in turn relies on improvements in financial market sentiment and stabilization in some of the larger currently-troubled emerging markets.

Danny Richards, Lead Economist at GlobalData, comments: “Some major advanced economies have struggled to generate growth momentum, including the US, the UK and Australia. In China, where the authorities are stepping up investment in infrastructure to prevent a continued slowdown, growth will remain positive, contributing to a slight acceleration in growth in total output in the emerging markets.”

Richards continues: “Geopolitical risks are intensifying, which could potentially undermine investor confidence and disrupt capital flows in the early part of the forecast period. Risks to the overall forecast stem primarily from a possible escalation in the trade war between the US and China, as well as inflamed tensions between the US and Iran following the recent drone strikes on Saudi Arabia’s largest oil processing center, which were blamed on Iran.

“The emerging markets of South-East Asia will invest heavily in new infrastructure projects, supported by private investment, and this region will be the fastest growing, expanding by 6.4% between 2019 and 2023.”

Information based on GlobalData’s report: ‘Global Construction Outlook to 2023 – Q3 2019 Update.

Related Stories

Market Data | Dec 5, 2021

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

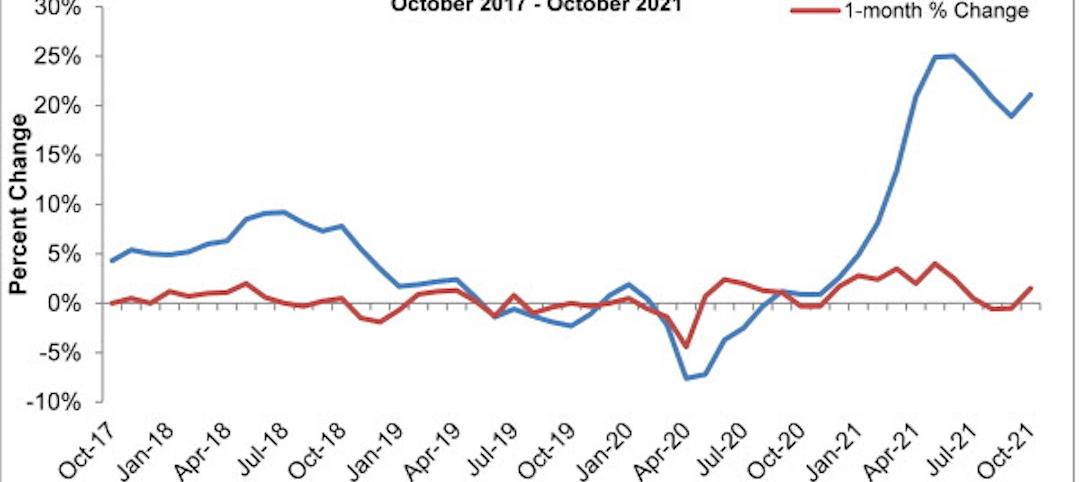

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

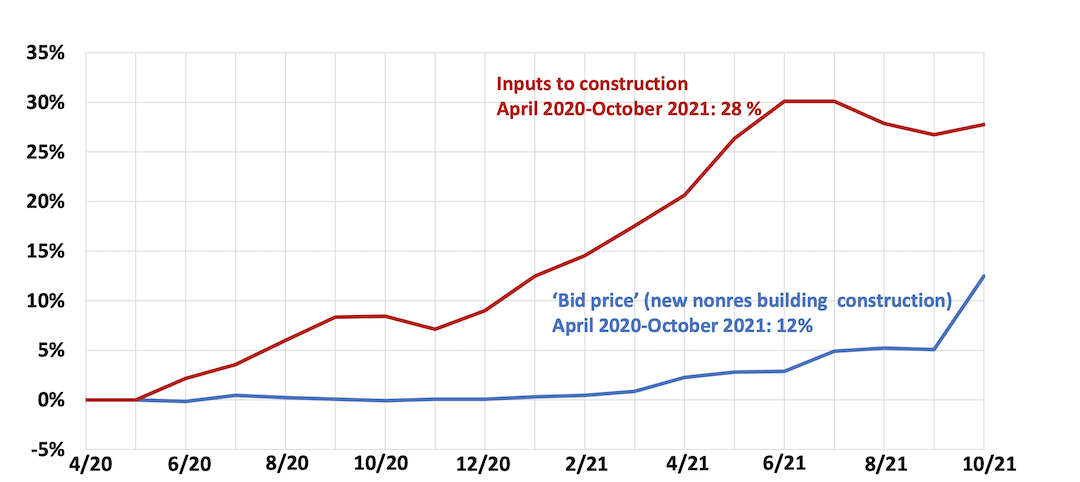

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.