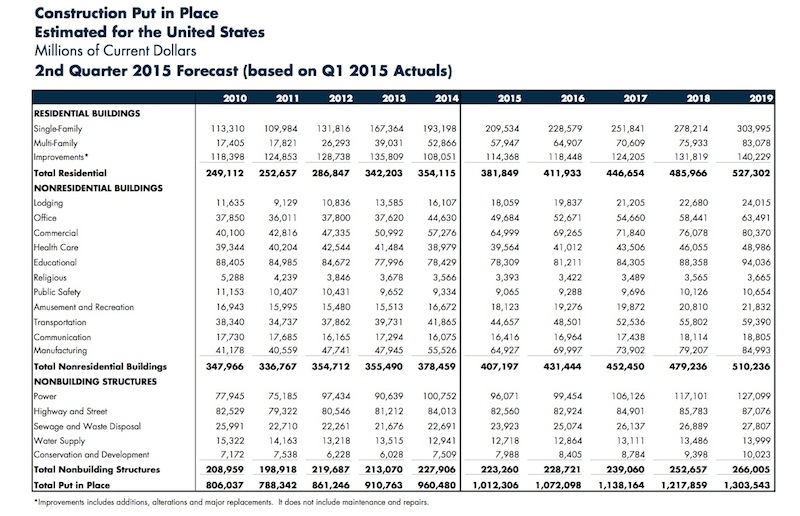

The United States is on track to end this year with its highest level of construction put in place since 2008, a total that, if achieved, would represent nearly 7% of the country’s GDP.

However, construction has slowed of late, according to FMI Corporation, the management and investment consultant. In its Q2 Construction Outlook, FMI estimates construction in place this year would rise 5% to $1.012 trillion. In the first quarter, FMI had projected an 8% annualized gain.

FMI estimates the nonresidential building portion of total construction to expand by 7.6% to $407.2 billion in 2015, and to keep growing through 2019, when it should reach $510.2 billion. However, with housing also expected to recover strongly during this period, nonresidential building’s share of total construction put in place would fall in 2019 to 39.1%, from 40.2% in 2015.

Construction spending in general “continues to build on the rapid growth experienced in the industry last year,” observes Chris Daum, FMI’s senior managing director and president of Investment Banking. FMI’s latest report looks at 17 sectors. Here are some highlights:

• Don’t anticipate much from the two big-ticket sectors, Healthcare and Education, says FMI.

Even with 2.5 million students expected to enroll over the next four year, FMI doesn’t see Education growing in 2015. “One of the biggest hurdles to new construction continues to be state and local budgets,” it writes, adding that there is likely to be “significantly less” state funding for K-12 schools.”

Healthcare should fare a little better, growing by 2% in 2015, and 4% in 2016 to $41 billion. But a “difficult funding environment,” along with changes to construction delivery methods, poses challenges. One trend FMI identifies is toward rebuilding existing facilities using modern hospital design and allow for greater use of technology.

• Manufacturing: After a double-digit gain in 2014, FMI expects manufacturing construction to increase by 17% this year, and then slow to an 8% increase in 2016. It cautions that manufacturing capital construction is highly cyclical when markets reach a state of overcapacity, as some petrochemical products are expected to do in the next few years after a spate of building.

• Amusement/recreation: This section grew by 7% in 2014, and should top that at 9% in 2015. Several major sports stadiums are under construction, and a number of smaller towns and colleges are improving their sports facilities. States also continue to welcome gaming in hopes of increasing their tax bases. A new mixed-use development model combines multiple entertainment venues and shopping into an overall plan.

• Lodging: This sector will be a bright spot, growing by 19% in 2015, and by 12% in 2016, before slowing to 7% in 2019. To buttress its projections, FMI quotes from Lodging Econometrics’ May 2015 reports, which notes that there are 3,885 projects with 488,230 rooms in the construction pipeline, “with the last three quarters posting Year-Over-Year gains of 20% or greater.”

• Office: This sector is benefiting from improving employment levels, and should see 11% growth in 2015, albeit a bit slower than the 19% it hit in 2014.

• Commercial: Capturing what’s going on in retail construction, this sector is expected to grow by 13% to $69 billion this year, but be flat in 2016. “Consumers remain relatively confident about the economy, but they are also remaining conservative in their discretionary spending, at least until wage recovery improves,” FMI writes.

• Religious: What growth there is will likely be in renovation, as new congregations move into vacated retail space or reoccupy church buildings abandoned by other faiths. FMI thinks this sector could be flatlining, and quotes statistics from Pew Research Center that show the percentage of adults (ages 18 and older) who describe themselves as Christians dropping by nearly eight percentage points in just seven years through 2014. Over that same period, the percentage of Americans who are religiously unaffiliated jumped by more than six points, to 22.8%

• Transportation: After registering 5% growth in 2014, transportation is expected to add 7% for 2015 to $44.7 billion. But this sector remains heavily dependent on government support that is never a certainty.

Related Stories

Coronavirus | May 29, 2020

Black & Veatch, DPR, Haskell, McCarthy launch COVID-19 construction safety coalition

The NEXT Coalition will challenge engineering and construction firms to enhance health and safety amid the Coronavirus pandemic.

Coronavirus | May 26, 2020

9 tips for mastering virtual public meetings during the COVID-19 pandemic

Mike Aziz, AIA, presents 9 tips for mastering virtual public meetings during the COVID-19 pandemic.

Coronavirus | May 18, 2020

Infection control in office buildings: Preparing for re-occupancy amid the coronavirus

Making workplaces safer will require behavioral resolve nudged by design.

Data Centers | May 8, 2020

Data centers as a service: The next big opportunity for design teams

As data centers compete to process more data with lower latency, the AEC industry is ideally positioned to develop design standards that ensure long-term flexibility.

Coronavirus | Apr 30, 2020

Gilbane shares supply-chain status of products affected by coronavirus

Imported products seem more susceptible to delays

Coronavirus | Apr 14, 2020

COVID-19 alert: Missouri’s first Alternate Care Facility ready for coronavirus patients

Missouri’s first Alternate Care Facility ready for coronavirus patients

AEC Tech | Apr 13, 2020

A robotic dog becomes part of Swinerton’s construction technology arsenal

Boston Dynamics, the robot’s creator, has about 100 machines in the field currently.

Coronavirus | Apr 8, 2020

COVID-19 alert: Most U.S. roofing contractors hit by coronavirus, says NRCA

NRCA survey shows 52% of roofing contractor said COVID-19 pandemic was having a significant or very significant impact on their businesses.

Coronavirus | Apr 5, 2020

COVID-19: Most multifamily contractors experiencing delays in projects due to coronavirus pandemic

The NMHC Construction Survey is intended to gauge the magnitude of the disruption caused by the COVID-19 outbreak on multifamily construction.