Commercial real estate brokers are optimistic about their industry’s growth prospects for 2019, according to a poll of brokers that Transwestern released last month. They are buoyed by strong consumer and business confidence, steady employment growth, and the anticipation of available debt and equity liquidity.

The survey explored the sentiments of brokerage professionals about three sectors: offices, medical offices, and industrial.

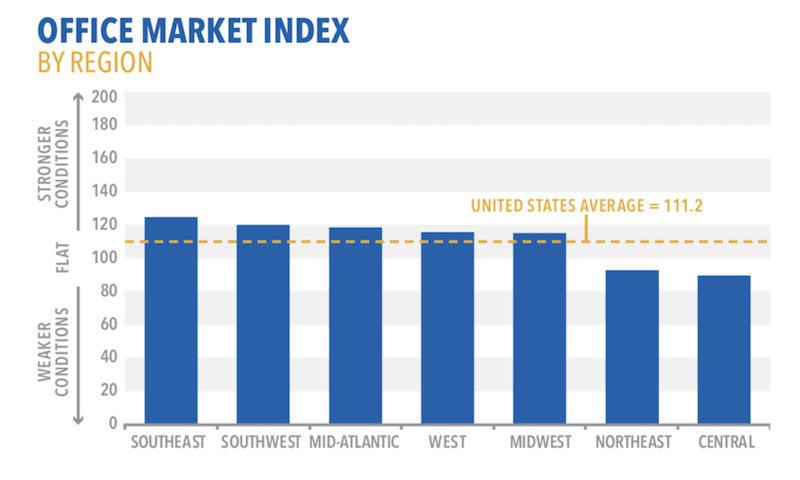

Over half of the 107 respondents, 52%, believe that leasing velocity, tenant walk throughs, and asking rents in the U.S. office market will be slightly to significantly higher in 2019. These factors will be driven primarily by continued economic expansion, lease expirations coming due, and rising interest rates.

Amenities continue to spur tenant interest, with access to transportation/parking and reliable WiFi service leading the “very important” list.

More than three quarters of respondents expect development levels to be flat or slightly higher in 2019, with select markets showing concern of oversupply and rising construction costs.

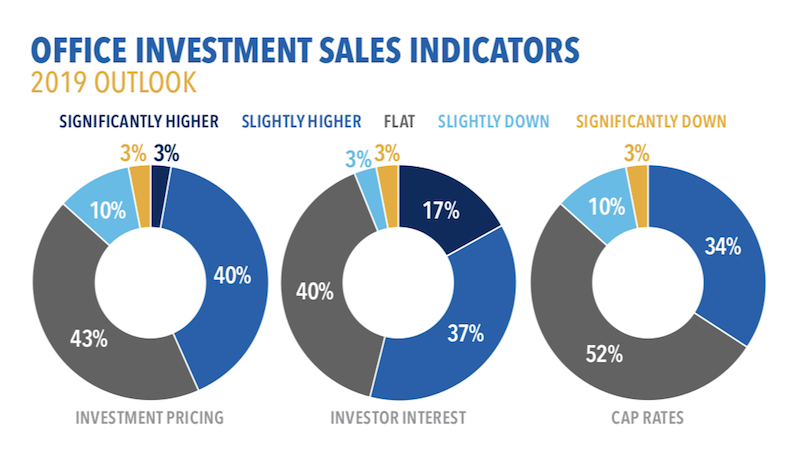

Most brokers foresee flat to modest growth for office pricing, investor interest and cap rates. Image: Transwestern

Nine of 10 respondents expect asking rents for medical offices to be slightly higher in 2019, driven by leasing activity. Demand is being driven by a growing and aging population. Cap rates in the medical office sector will be flat compared to 2018, predict 80% of respondents, with most also expecting investor interest to rise over the year.

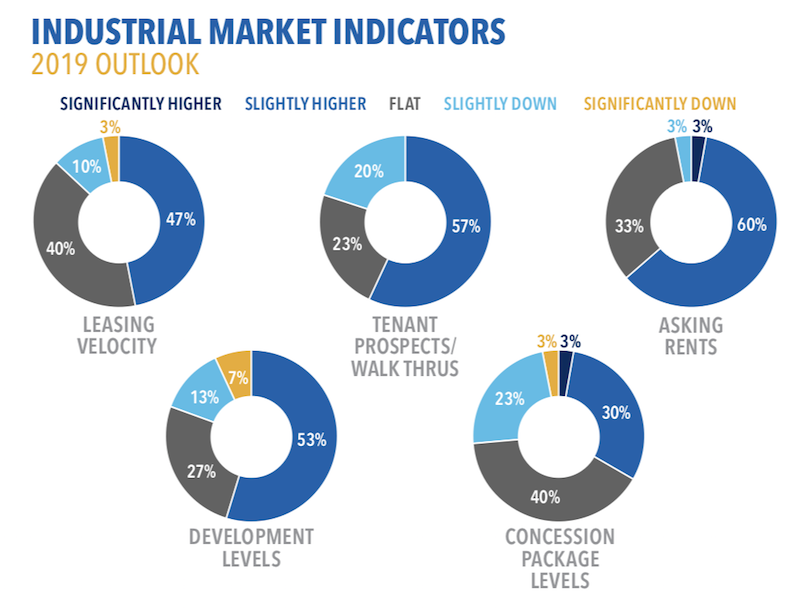

While the average index of 122.1 for the industrial sector’s prospects next year was down from 130.9 for last year’s outlook, respondents still expect tenant walk throughs, asking rents, and development to be higher for this sector, driven by ecommerce, a growing population demanding consumer goods, and better economic conditions.

Seventy-two percent of respondents expect higher investment interest in 2019, as the industrial market strengthens and select REITs shift focus away from office to industrial properties, especially in the Northeast and Mid-Atlantic regions.

Brokers expect an uptick next year, particularly in asking rents and tenant prospects, for the industrial sector. Image: Transwestern

Brokers expect an uptick next year, particularly in asking rents and tenant prospects, for the industrial sector. Image: Transwestern

Related Stories

Market Data | Dec 13, 2022

Contractors' backlog of work reaches three-year high

U.S. construction firms have, on average, 9.2 months of work in the pipeline, according to ABC's latest Construction Backlog Indicator.

Contractors | Dec 6, 2022

Slow payments cost the construction industry $208 billion in 2022

The cost of floating payments for wages and invoices represents $208 billion in excess cost to the construction industry, a 53% increase from 2021, according to a survey by Rabbet, a provider of construction finance software.

Mass Timber | Dec 1, 2022

Cross laminated timber market forecast to more than triple by end of decade

Cross laminated timber (CLT) is gaining acceptance as an eco-friendly building material, a trend that will propel its growth through the end of the 2020s. The CLT market is projected to more than triple from $1.11 billion in 2021 to $3.72 billion by 2030, according to a report from Polaris Market Research.

Market Data | Nov 15, 2022

Construction demand will be a double-edged sword in 2023

Skanska’s latest forecast sees shorter lead times and receding inflation, but the industry isn’t out of the woods yet.

Reconstruction & Renovation | Nov 8, 2022

Renovation work outpaces new construction for first time in two decades

Renovations of older buildings in U.S. cities recently hit a record high as reflected in architecture firm billings, according to the American Institute of Architects (AIA).

Market Data | Nov 3, 2022

Building material prices have become the calm in America’s economic storm

Linesight’s latest quarterly report predicts stability (mostly) through the first half of 2023

Building Team | Nov 1, 2022

Nonresidential construction spending increases slightly in September, says ABC

National nonresidential construction spending was up by 0.5% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Hotel Facilities | Oct 31, 2022

These three hoteliers make up two-thirds of all new hotel development in the U.S.

With a combined 3,523 projects and 400,490 rooms in the pipeline, Marriott, Hilton, and InterContinental dominate the U.S. hotel construction sector.

Codes and Standards | Oct 26, 2022

‘Landmark study’ offers key recommendations for design-build delivery

The ACEC Research Institute and the University of Colorado Boulder released what the White House called a “landmark study” on the design-build delivery method.

Building Team | Oct 26, 2022

The U.S. hotel construction pipeline shows positive growth year-over-year at Q3 2022 close

According to the third quarter Construction Pipeline Trend Report for the United States from Lodging Econometrics (LE), the U.S. construction pipeline stands at 5,317 projects/629,489 rooms, up 10% by projects and 6% rooms Year-Over-Year (YOY).