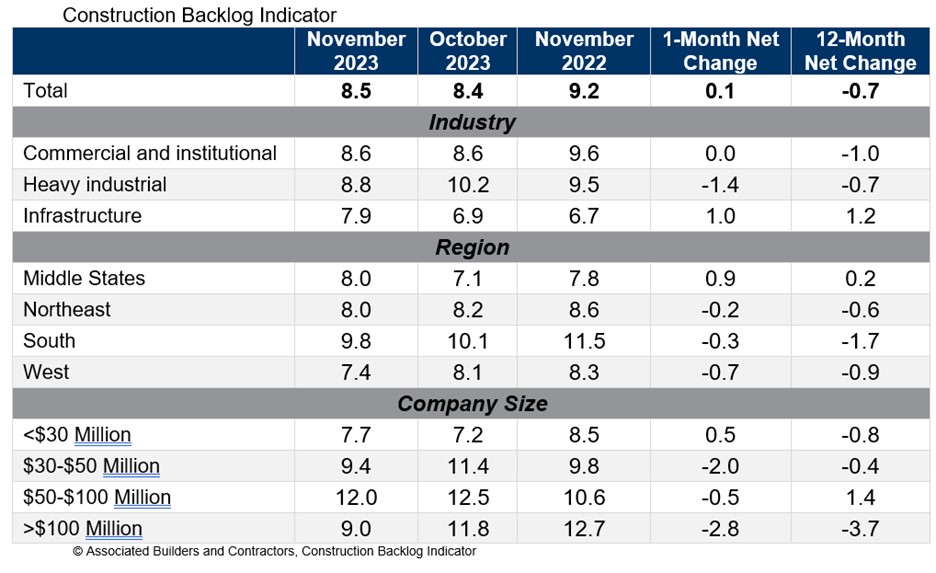

Associated Builders and Contractors reported today that its Construction Backlog Indicator inched up to 8.5 months in November from 8.4 months in October, according to an ABC member survey conducted Nov. 20 to Dec. 4. The reading is down 0.7 months from November 2022.

View ABC’s Construction Backlog Indicator and Construction Confidence Index tables for November. View the full Construction Backlog Indicator and Construction Confidence Index data series.

Despite the monthly increase, backlog is currently 0.8 months lower than at July’s cyclical peak. The sharpest declines over that span occurred among contractors with more than $100 million in annual revenues, who collectively reported fewer than 10 months of backlog in November for the first time since the second quarter of 2018.

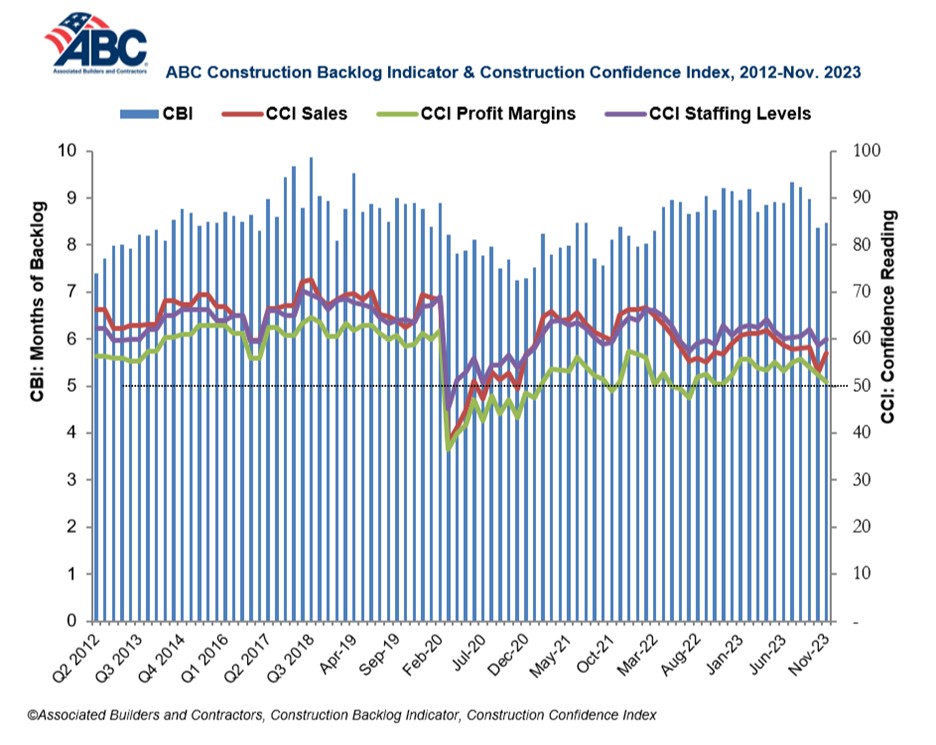

ABC’s Construction Confidence Index readings for sales and staffing levels increased in November, while the reading for profit margins fell. All three readings remain above the threshold of 50, indicating expectations for growth over the next six months.

“A growing number of contractors are reporting declines in backlog,” said ABC Chief Economist Anirban Basu. “The interest rate hikes implemented by the Federal Reserve appear to be making more of a mark on the economy. Not only has the cost of capital risen over the past 20+ months, but credit conditions are also tightening, rendering project financing even more challenging.

“The good news is that certain interest rates have begun to fall in anticipation of Federal Reserve rate cuts next year, perhaps as early as the first quarter,” said Basu. “Still, 2024 is poised to be weaker from a construction demand perspective for many firms, especially those that depend heavily on private developers. Those operating in public construction and/or industrial segments should meet with less resistance on average.”

Related Stories

Airports | Aug 31, 2015

Experts discuss how airports can manage growth

In February 2015, engineering giant Arup conducted a “salon” in San Francisco on the future of aviation. This report provides an insight into their key findings.

Healthcare Facilities | Aug 28, 2015

Hospital construction/renovation guidelines promote sound control

The newly revised guidelines from the Facilities Guidelines Institute touch on six factors that affect a hospital’s soundscape.

steps toward a quieter hospital")

Healthcare Facilities | Aug 28, 2015

7 (more) steps toward a quieter hospital

Every hospital has its own “culture” of loudness and quiet. Jacobs’ Chris Kay offers steps to a therapeutic auditory environment.

Healthcare Facilities | Aug 28, 2015

Shhh!!! 6 ways to keep the noise down in new and existing hospitals

There’s a ‘decibel war’ going on in the nation’s hospitals. Progressive Building Teams are leading the charge to give patients quieter healing environments.

Mixed-Use | Aug 26, 2015

Innovation districts + tech clusters: How the ‘open innovation’ era is revitalizing urban cores

In the race for highly coveted tech companies and startups, cities, institutions, and developers are teaming to form innovation hot pockets.

Contractors | Aug 19, 2015

FMI's Nonresidential Construction Index Report: Recovery continues despite slow down

The Q3 NRCI dropped to 63.6 from the previous reading of 64.9 in Q2, painting a mixed picture of the state of the nonresidential construction sector.

Giants 400 | Aug 7, 2015

GOVERNMENT SECTOR GIANTS: Public sector spending even more cautiously on buildings

AEC firms that do government work say their public-sector clients have been going smaller to save money on construction projects, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

K-12 SCHOOL SECTOR GIANTS: To succeed, school design must replicate real-world environments

Whether new or reconstructed, schools must meet new demands that emanate from the real world and rapidly adapt to different instructional and learning modes, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

MULTIFAMILY AEC GIANTS: Slowdown prompts developers to ask: Will the luxury rentals boom hold?

For the last three years, rental apartments have occupied the hot corner in residential construction, as younger people gravitated toward renting to be closer to urban centers and jobs. But at around 360,000 annual starts, multifamily might be peaking, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

UNIVERSITY SECTOR GIANTS: Collaboration, creativity, technology—hallmarks of today’s campus facilities

At a time when competition for the cream of the student/faculty crop is intensifying, colleges and universities must recognize that students and parents are coming to expect an education environment that foments collaboration, according to BD+C's 2015 Giants 300 report.