Financing solutions provider Billd recently surveyed nearly 900 commercial construction professionals across the U.S. for its 2023 National Subcontractor Market Report. Its key finding: rising input prices for materials and labor cost subcontractors $97 billion in unplanned expenses last year.

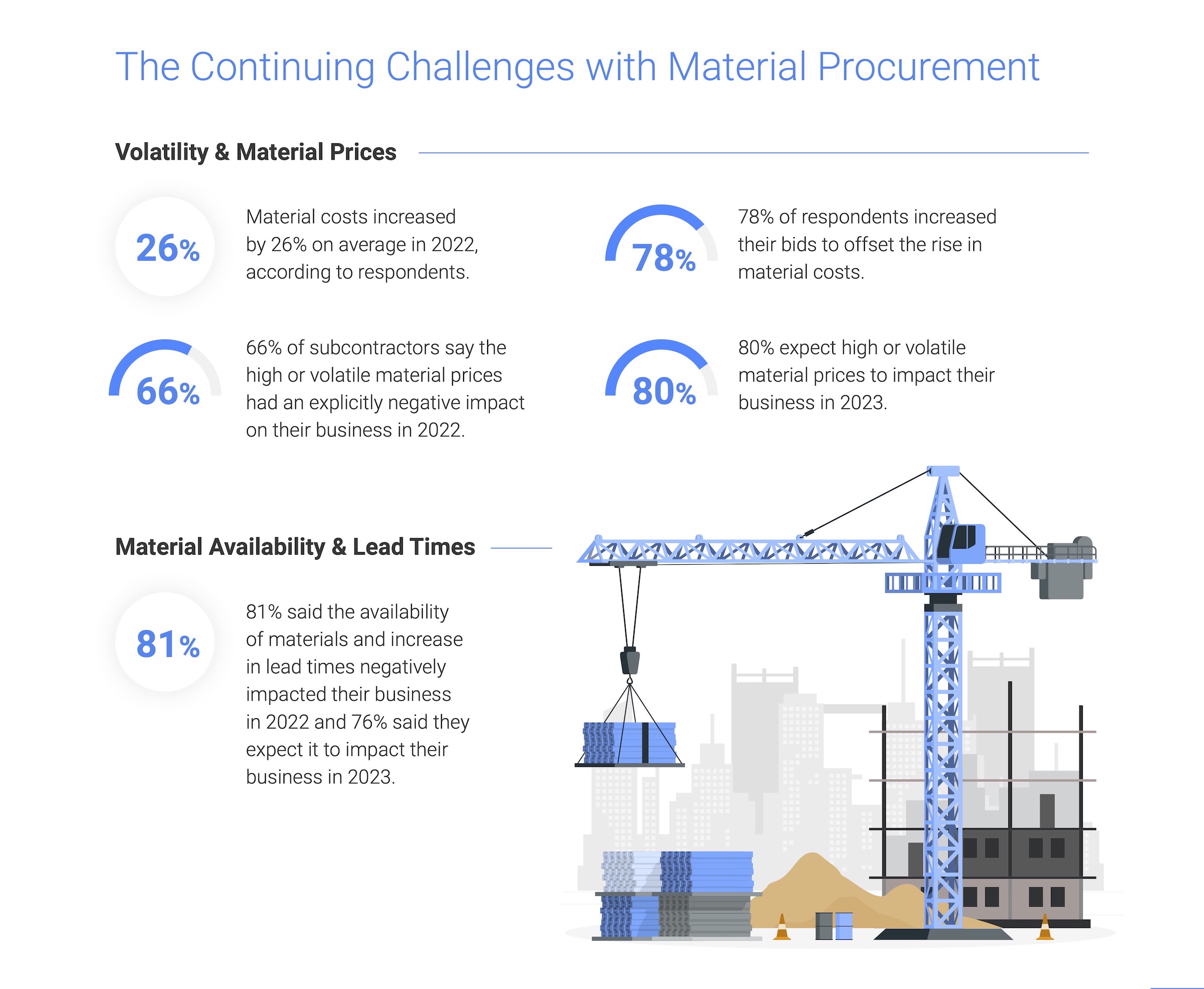

Rising material costs and price volatility are not new issues for subcontractors, with 81% of those surveyed reporting a negative effect on their businesses in 2022; 80% expect that trend to continue. It is no surprise given material costs jumped a staggering 26%, according to respondents. Similarly, competition for labor due to the longtime labor shortage was validated by a 15% average increase in labor cost. Together, those increases amounted to $97 billion in additional expenses for the subcontractor. While some subcontractors increased their bids to offset these rapidly rising costs, one third of respondents were unable to raise those bids commensurate with their expenses. This resulted in 57% of businesses reporting a decrease in profitability, despite 61% reporting revenue growth.

"Subcontractors are the foundation of the construction industry, providing all material and labor to complete a project," said Chris Doyle, CEO of Billd. "They purchase that material and pay for that labor upfront, not being paid for their work for 74 days, a result of the dysfunctional payment cycle. If you add unplanned expenses due to rising costs in material and labor, it puts an unrealistic burden on subcontractors to provide that foundation."

The report examines how macroeconomic conditions from this and prior years impacted subcontractors in 2022, as well as their outlook for 2023. It also creates hope by providing perspective on new financing options subcontractors can leverage as mainstays – like supplier terms – become less reliable. 72% of respondents report having supplier terms of 30 days or less. Compared to a 74-day average wait time for payment, it is no surprise that 51% deem the length of their terms insufficient.

Supplier terms also have an unforeseen cost; most suppliers (also surveyed) state that they offer discounts for upfront payment. Despite those disadvantages, 87% of respondents still rely on supplier terms as their predominant means of buying materials. When it comes to funding their increasing labor costs, traditional financing options are even less accessible, leaving 87% of respondents coming out of pocket for labor before getting paid themselves. Luckily, the report highlights financial relief for labor as well as materials.

Related Stories

| Dec 3, 2013

Historic Daytona International Speedway undergoing $400 million facelift

The Daytona International Speedway is zooming ahead on the largest renovation in the Florida venue’s 54-year history. Improvements include five redesigned guest entrances, an extended grandstand with 101,000 new seats, and more than 60 new trackside suites for corporate entertaining.

| Dec 3, 2013

Creating a healthcare capital project plan: The truth behind the numbers

When setting up a capital project plan, it's one thing to have the data, but quite another to have the knowledge of the process.

| Dec 3, 2013

Architects urge government to reform design-build contracting process

Current federal contracting laws are discouraging talented architects from competing for federal contracts, depriving government and, by inference, taxpayers of the best design expertise available, according to AIA testimony presented today on Capitol Hill.

| Dec 3, 2013

Construction spending hits four-year peak after rare spike in public outlays

An unusual surge in public construction in October pushed total construction spending to its highest level since May 2009 despite a dip in both private residential and nonresidential activity.

| Nov 27, 2013

BIG's 'oil and vinegar' design wins competition for the Museum of the Human Body [slideshow]

The winning submission by Bjarke Ingels Group (BIG) and A+ Architecture mixes urban pavement and parkland in a flowing, organic plan, like oil and vinegar, explains Bjarke Ingels.

| Nov 27, 2013

Retail renaissance: What's next?

The retail construction category, long in the doldrums, is roaring back to life. Send us your comments and projects as we prepare coverage for this exciting sector.

| Nov 27, 2013

Pediatric hospitals improve care with flexible, age-sensitive design

Pediatric hospitals face many of the same concerns as their adult counterparts. Inpatient bed demand is declining, outpatient visits are soaring, and there is a higher level of focus on prevention and reduced readmissions.

| Nov 27, 2013

Exclusive survey: Revenues increased at nearly half of AEC firms in 2013

Forty-six percent of the respondents to an exclusive BD+C survey of AEC professionals reported that revenues had increased this year compared to 2012, with another 24.2% saying cash flow had stayed the same.

| Nov 27, 2013

Wonder walls: 13 choices for the building envelope

BD+C editors present a roundup of the latest technologies and applications in exterior wall systems, from a tapered metal wall installation in Oklahoma to a textured precast concrete solution in North Carolina.

| Nov 27, 2013

University reconstruction projects: The 5 keys to success

This AIA CES Discovery course discusses the environmental, economic, and market pressures affecting facility planning for universities and colleges, and outlines current approaches to renovations for critical academic spaces.