Financing solutions provider Billd recently surveyed nearly 900 commercial construction professionals across the U.S. for its 2023 National Subcontractor Market Report. Its key finding: rising input prices for materials and labor cost subcontractors $97 billion in unplanned expenses last year.

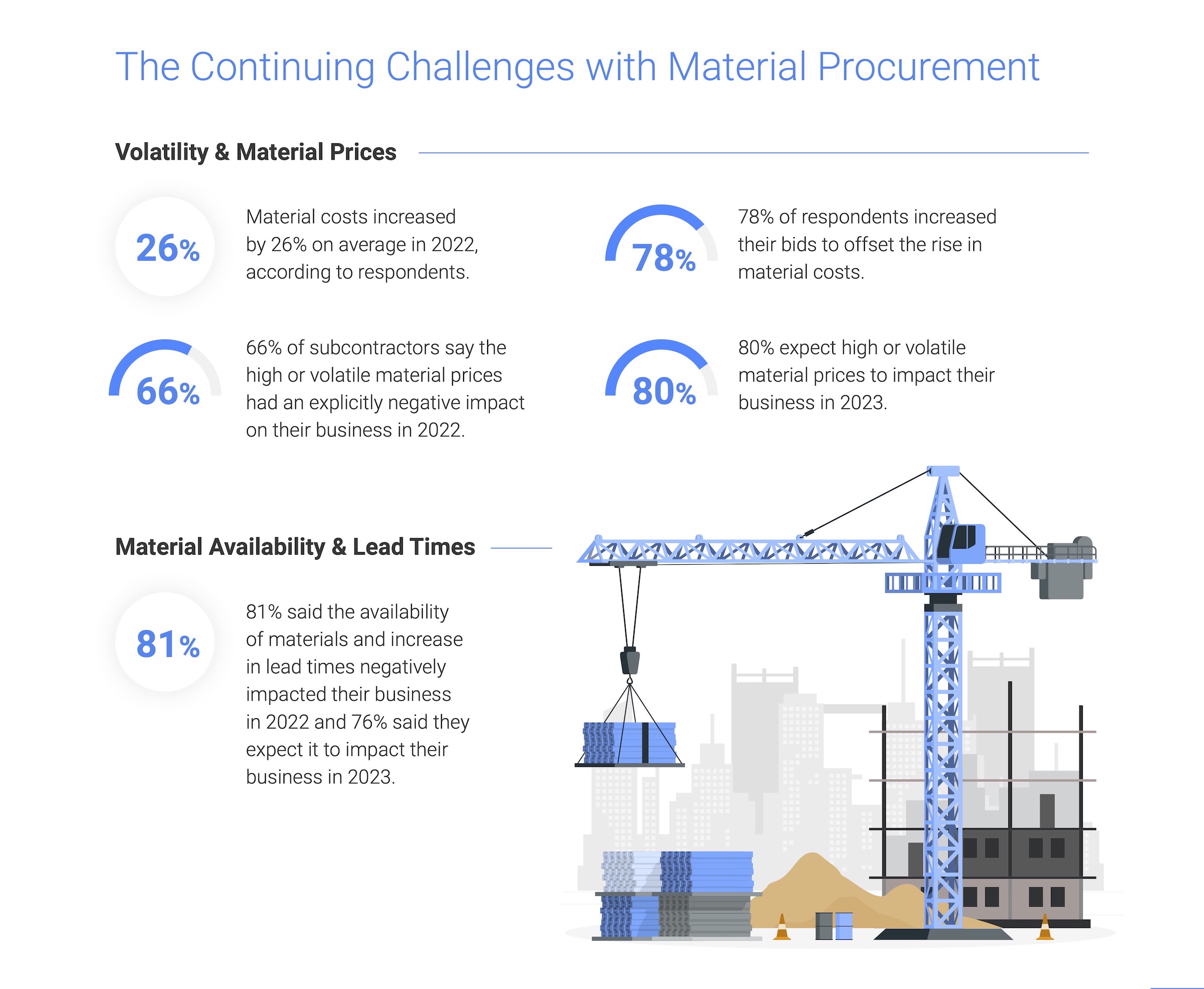

Rising material costs and price volatility are not new issues for subcontractors, with 81% of those surveyed reporting a negative effect on their businesses in 2022; 80% expect that trend to continue. It is no surprise given material costs jumped a staggering 26%, according to respondents. Similarly, competition for labor due to the longtime labor shortage was validated by a 15% average increase in labor cost. Together, those increases amounted to $97 billion in additional expenses for the subcontractor. While some subcontractors increased their bids to offset these rapidly rising costs, one third of respondents were unable to raise those bids commensurate with their expenses. This resulted in 57% of businesses reporting a decrease in profitability, despite 61% reporting revenue growth.

"Subcontractors are the foundation of the construction industry, providing all material and labor to complete a project," said Chris Doyle, CEO of Billd. "They purchase that material and pay for that labor upfront, not being paid for their work for 74 days, a result of the dysfunctional payment cycle. If you add unplanned expenses due to rising costs in material and labor, it puts an unrealistic burden on subcontractors to provide that foundation."

The report examines how macroeconomic conditions from this and prior years impacted subcontractors in 2022, as well as their outlook for 2023. It also creates hope by providing perspective on new financing options subcontractors can leverage as mainstays – like supplier terms – become less reliable. 72% of respondents report having supplier terms of 30 days or less. Compared to a 74-day average wait time for payment, it is no surprise that 51% deem the length of their terms insufficient.

Supplier terms also have an unforeseen cost; most suppliers (also surveyed) state that they offer discounts for upfront payment. Despite those disadvantages, 87% of respondents still rely on supplier terms as their predominant means of buying materials. When it comes to funding their increasing labor costs, traditional financing options are even less accessible, leaving 87% of respondents coming out of pocket for labor before getting paid themselves. Luckily, the report highlights financial relief for labor as well as materials.

Related Stories

Airports | Aug 31, 2015

Experts discuss how airports can manage growth

In February 2015, engineering giant Arup conducted a “salon” in San Francisco on the future of aviation. This report provides an insight into their key findings.

Healthcare Facilities | Aug 28, 2015

Hospital construction/renovation guidelines promote sound control

The newly revised guidelines from the Facilities Guidelines Institute touch on six factors that affect a hospital’s soundscape.

steps toward a quieter hospital")

Healthcare Facilities | Aug 28, 2015

7 (more) steps toward a quieter hospital

Every hospital has its own “culture” of loudness and quiet. Jacobs’ Chris Kay offers steps to a therapeutic auditory environment.

Healthcare Facilities | Aug 28, 2015

Shhh!!! 6 ways to keep the noise down in new and existing hospitals

There’s a ‘decibel war’ going on in the nation’s hospitals. Progressive Building Teams are leading the charge to give patients quieter healing environments.

Mixed-Use | Aug 26, 2015

Innovation districts + tech clusters: How the ‘open innovation’ era is revitalizing urban cores

In the race for highly coveted tech companies and startups, cities, institutions, and developers are teaming to form innovation hot pockets.

Contractors | Aug 19, 2015

FMI's Nonresidential Construction Index Report: Recovery continues despite slow down

The Q3 NRCI dropped to 63.6 from the previous reading of 64.9 in Q2, painting a mixed picture of the state of the nonresidential construction sector.

Giants 400 | Aug 7, 2015

GOVERNMENT SECTOR GIANTS: Public sector spending even more cautiously on buildings

AEC firms that do government work say their public-sector clients have been going smaller to save money on construction projects, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

K-12 SCHOOL SECTOR GIANTS: To succeed, school design must replicate real-world environments

Whether new or reconstructed, schools must meet new demands that emanate from the real world and rapidly adapt to different instructional and learning modes, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

MULTIFAMILY AEC GIANTS: Slowdown prompts developers to ask: Will the luxury rentals boom hold?

For the last three years, rental apartments have occupied the hot corner in residential construction, as younger people gravitated toward renting to be closer to urban centers and jobs. But at around 360,000 annual starts, multifamily might be peaking, according to BD+C's 2015 Giants 300 report.

Giants 400 | Aug 7, 2015

UNIVERSITY SECTOR GIANTS: Collaboration, creativity, technology—hallmarks of today’s campus facilities

At a time when competition for the cream of the student/faculty crop is intensifying, colleges and universities must recognize that students and parents are coming to expect an education environment that foments collaboration, according to BD+C's 2015 Giants 300 report.