A recent survey of more than 200 subcontractors and suppliers in the Northeast found that respondents have been prefabricating 20% more than they did prior to the COVID-19 pandemic. And 71% said that they had seen an increase in requests for design-assist proposals, a strong sign that speed-to-market is a priority.

Consigli Construction’s Market Outlook Report for the first and second quarters of 2021 states that the pandemic has motivated subs and vendors to turn to technology in their shops and field processes. The survey’s respondents are also more receptive to cost-saving material management software, tool upgrades, and robotics that improve efficiency and give subs the flexibility they need to manage on-site workforces at a time when skilled labor is in short supply in some markets.

While 72% of the survey’s respondents say they aren’t concerned about staffing their projects this year, Consigli suggests they need to monitor their workforce resources for 2022, based on the amount of work in the pipeline.

PRICING AND SUPPLY ARE ISSUES FOR SEVERAL PRODUCT

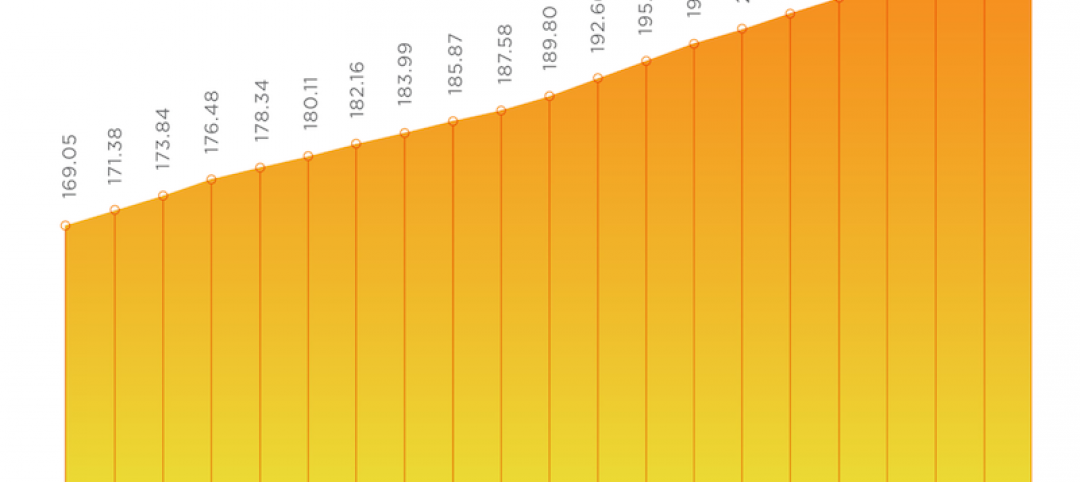

The Market Outlook expects copper and steel to manifest the greatest risk for price inflation. Chart: Consigli Construction

The Market Outlook Report also looks at materials price inflation in several product categories (see chart). Metal studs, copper, and PVC are the materials that the report expects to show the greatest price increases in the first half of the year. The report also suggests that lumber—whose pricing had jumped by 73% since February 2020—could be stabilizing, depending on residential demand.

(The Commerce Department reported last week that housing starts had surged to a nearly 15-year high in March.)

Consigli recommends that subs keep a close eye on high-risk materials, and lock in prices as soon as possible to avoid exposure to inflation. Subs should also watch for supply-chain disruptions, especially for products coming from overseas like flooring and cabinetry. Where possible, have access to alternate materials and delivery options.

Related Stories

Market Data | Jan 19, 2021

2021 construction forecast: Nonresidential building spending will drop 5.7%, bounce back in 2022

Healthcare and public safety are the only nonresidential construction sectors that will see growth in spending in 2021, according to AIA's 2021 Consensus Construction Forecast.

Market Data | Jan 13, 2021

Atlanta, Dallas seen as most favorable U.S. markets for commercial development in 2021, CBRE analysis finds

U.S. construction activity is expected to bounce back in 2021, after a slowdown in 2020 due to challenges brought by COVID-19.

Market Data | Jan 13, 2021

Nonres construction could be in for a long recovery period

Rider Levett Bucknall’s latest cost report singles out unemployment and infrastructure spending as barometers.

Market Data | Jan 13, 2021

Contractor optimism improves as ABC’s Construction Backlog inches up in December

ABC’s Construction Confidence Index readings for sales, profit margins, and staffing levels increased in December.

Market Data | Jan 11, 2021

Turner Construction Company launches SourceBlue Brand

SourceBlue draws upon 20 years of supply chain management experience in the construction industry.

Market Data | Jan 8, 2021

Construction sector adds 51,000 jobs in December

Gains are likely temporary as new industry survey finds widespread pessimism for 2021.

Market Data | Jan 7, 2021

Few construction firms will add workers in 2021 as industry struggles with declining demand, growing number of project delays and cancellations

New industry outlook finds most contractors expect demand for many categories of construction to decline.

Market Data | Jan 5, 2021

Barely one-third of metros add construction jobs in latest 12 months

Dwindling list of project starts forces contractors to lay off workers.

Market Data | Jan 4, 2021

Nonresidential construction spending shrinks further in November

Many commercial projects languish, even while homebuilding soars.

Market Data | Dec 29, 2020

Multifamily transactions drop sharply in 2020, according to special report from Yardi Matrix

Sales completions at end of Q3 were down over 41 percent from the same period a year ago.