Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

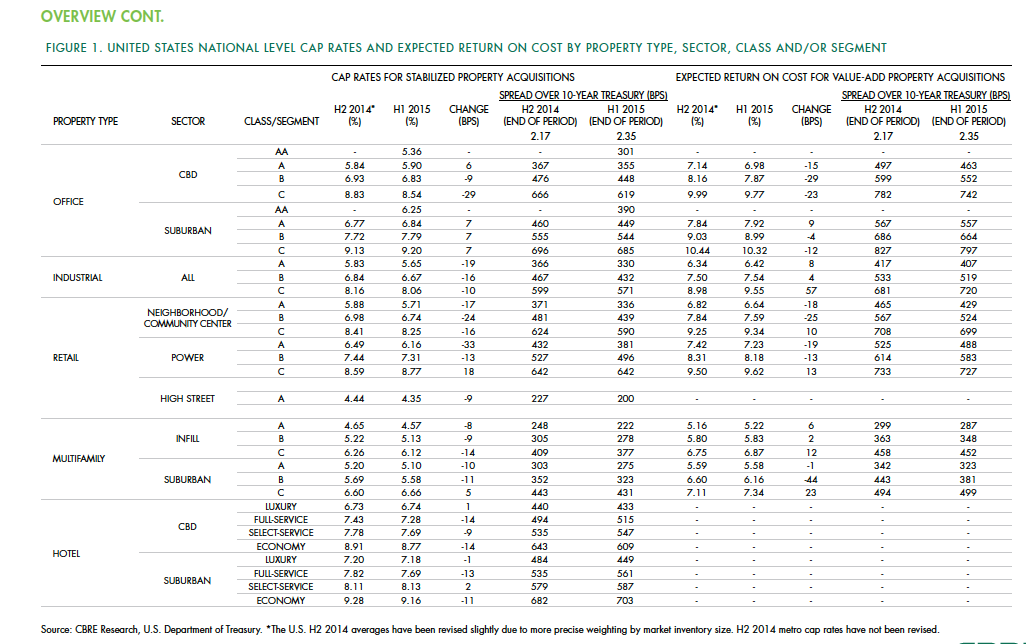

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Hotel Facilities | May 5, 2021

AC Hotel Fort Lauderdale Sawgrass Mills/Sunrise completes

Stantec designed the project.

Hotel Facilities | Apr 21, 2021

First newly constructed Signia by Hilton Hotel to be built in Atlanta

Signia by Hilton is a new upscale brand from Hilton Worldwide Holdings Inc.

AEC Tech | Mar 4, 2021

The Weekly show, March 4, 2021: Bringing AI to the masses, and Central Station Memphis hotel

This week on The Weekly show, BD+C editors speak with AEC industry leaders about the award-winning Central Station Memphis hotel reconstruction project, and how Autodesk aims to bring generative design and AI tools to the AEC masses.

Market Data | Feb 24, 2021

2021 won’t be a growth year for construction spending, says latest JLL forecast

Predicts second-half improvement toward normalization next year.

Hotel Facilities | Feb 16, 2021

Santa Monica Professional Building restored into a modern hotel

Howard Laks Architects designed the project.

Modular Building | Jan 26, 2021

Offsite manufacturing startup iBUILT positions itself to reduce commercial developers’ risks

iBUILT plans to double its production capacity this year, and usher in more technology and automation to the delivery process.

Daylighting | Jan 16, 2021

Daylighting system creates 'an oasis in the city' for renovated hotel in downtown Minneapolis

Solatube daylighting systems were used to bring natural light into the lobby of the Midland Bank building in Minneapolis.

Giants 400 | Dec 16, 2020

Download a PDF of all 2020 Giants 400 Rankings

This 70-page PDF features AEC firm rankings across 51 building sectors, disciplines, and specialty services.

Giants 400 | Dec 3, 2020

2020 Hotel Sector Giants: Top architecture, engineering, and construction firms in the U.S. hospitality sector

Gensler, Jacobs, and Suffolk Construction top BD+C's rankings of the nation's largest hotel sector architecture, engineering, and construction firms, as reported in the 2020 Giants 400 Report.