National nonresidential construction spending expanded 0.7% in August to its highest level since the U.S. Census Bureau began the data series in 2002, according to an Associated Builders and Contractors analysis released today.

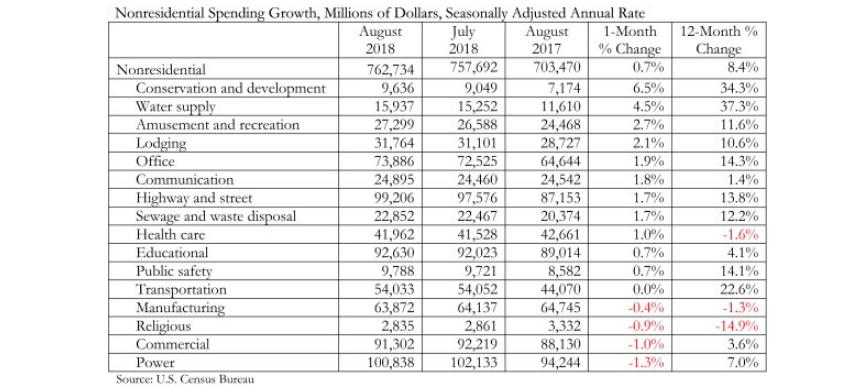

Total nonresidential spending stood at $762.7 billion on a seasonally adjusted, annualized rate in August, which represents an increase of 8.4% compared to one year ago. Private nonresidential spending fell 0.2% in August largely due to a 1.3% decline in power-related spending, the largest private construction spending category, and public nonresidential spending increased 2%.

“The good news on the nation’s economy and the construction sector just keeps coming,” said ABC Chief Economist Anirban Basu. “The increase in overall nonresidential construction spending was reasonably predictable given the predominance of positive leading indicators such as ABC’s Construction Backlog Indicator, which reported record-setting 9.9 months of backlog in the second quarter of this year, and the Architectural Billings Index. In addition, the recent pattern of stable private construction spending coupled with growing public spending remained in place in August.

“Rising property values, ongoing rapid job creation and a confident consumer translates into rising real estate values, income and retail sales tax collections, which in turn creates additional resources to invest in infrastructure,” said Basu. “That helps explain the chunky year-over-year spending increases in a number of primarily publicly financed categories, including water supply, which increased 37%; conservation and development, 34%; transportation, 23%; and highway/street, 14%.

“It is quite possible that construction spending growth will accelerate from current levels,” said Basu. “Aside from the strong economy, ongoing increases in materials prices and worker compensation is translating into rising project delivery costs, which, all things being equal, produces faster construction spending growth.

“For now, rising construction and borrowing costs are not stifling economic activity,” said Basu. “However, purchasers of construction services may be increasingly inclined to postpone projects if costs continue to rise, which is likely. And while contractors remain concerned about the overall construction workforce shortage negatively affecting project deadlines, the near-term outlook remains robust.”

Related Stories

| Jul 20, 2012

Office Report: Fitouts, renovations keep sector moving

BD+C's Giants 300 Top 25 AEC Firms in the Office sector.

| Jul 20, 2012

K-12 Schools Report: ‘A lot of pent-up need,’ with optimism for ’13

The Giants 300 Top 25 AEC Firms in the K-12 Schools Sector.

| Jul 20, 2012

Higher education market holding steady

But Giants 300 University AEC Firms aren’t expecting a flood of new work.

| Jul 20, 2012

3 important trends in hospital design that Healthcare Giants are watching closely

BD+C’s Giants 300 reveals top AEC firms in the healthcare sector.

| Jul 20, 2012

Global boom for hotels; for retail, not so much

The Giants 300 Top 10 Firms in the Hospitality and Retail sectors.

| Jul 20, 2012

Gensler, Stantec, Turner lead ‘green’ firms

The Top 10 AEC Firms in Green Buildings and LEED Accredited Staff.

. The church was founded in 1628,. In the last")

| Jul 19, 2012

Renovation resurgence cuts across sectors

Giants 300 reconstruction sector firms ‘pumping fresh blood in tired spaces.’

| Jul 19, 2012

AEC firms ready to dive into public projects

But the size of the pool keeps shrinking for the Top 25 AEC firms in the Government Sector.

| Jul 19, 2012

BIM finally starting to pay off for AEC firms

In surveying Giants 300 firms about BIM, we went right for the jugular: Is BIM paying off—through cost savings, higher quality, or client satisfaction? Here’s what they told us.