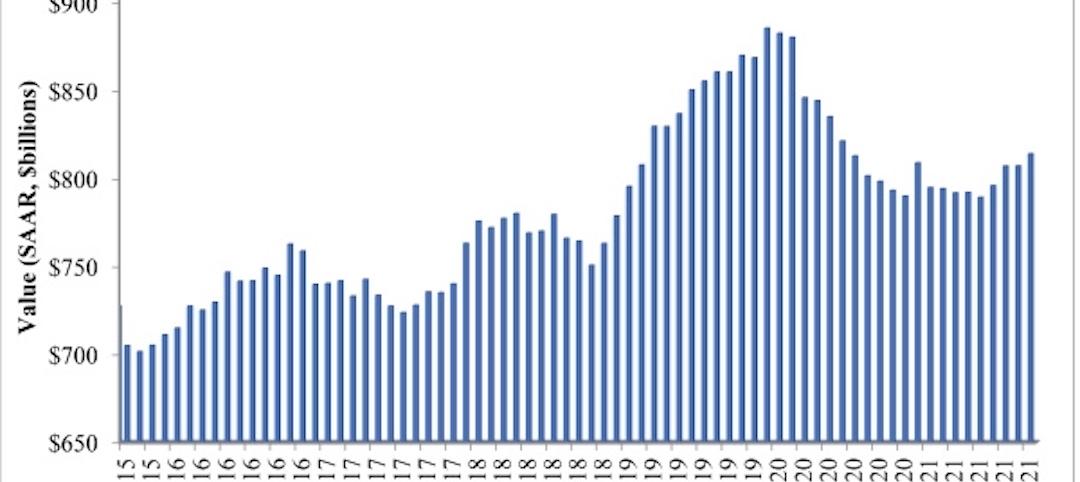

National nonresidential construction spending increased by 1.6% in January and is up 5.1% on a year-ago basis, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, spending totaled a record $806.9 billion in January.

Private nonresidential spending rose 0.8% on a monthly basis and is up 0.5% compared to the same time last year. Public nonresidential construction spending also increased, rising 2.6% for the month and 12.3% on a year over year basis.

“Despite all the focus on the dislocating impacts of the coronavirus, construction—a key element of the U.S. economy—continues to perform,” said ABC Chief Economist Anirban Basu. “For the first time in history, the volume of nonresidential construction spending exceeded $800 billion on an annualized basis and now stands at an all-time high. Both public and private nonresidential construction spending expanded to start 2020, a reflection of the broader economic momentum evident over the last several years. Backlog remains healthy, according to the ABC Construction Backlog Indicator, and with the nation continuing to add jobs, there is more demand for public and private construction and additional funding resources. This is especially apparent in several infrastructure categories, in which spending growth continues to be robust due to healthier state and local government finances.

“That said, there is no question that the coronavirus has significantly compromised both global and national economic momentum over the past two to three weeks,” said Basu. “U.S. manufacturing and shipping segments have begun to soften, with significant reductions in container volume already being reported at several major U.S. ports. While the crisis is expansive enough to potentially drive the economy into recession, the question is whether the crisis is severe enough to countervail current U.S. economic momentum.

“At this time, it is unclear how coronavirus will affect materials prices,” said Basu. “Certain construction components, whether from China or elsewhere, may experience inadequate supply during the weeks ahead, and the more general impact will be decreased input prices due to lower demand. This is likely to be the case for a number of key commodities, including those related to energy.”

Related Stories

Market Data | Dec 22, 2021

Two out of three metro areas add construction jobs from November 2020 to November 2021

Construction employment increased in 237 or 66% of 358 metro areas over the last 12 months.

Market Data | Dec 17, 2021

Construction jobs exceed pre-pandemic level in 18 states and D.C.

Firms struggle to find qualified workers to keep up with demand.

Market Data | Dec 15, 2021

Widespread steep increases in materials costs in November outrun prices for construction projects

Construction officials say efforts to address supply chain challenges have been insufficient.

Market Data | Dec 15, 2021

Demand for design services continues to grow

Changing conditions could be on the horizon.

Market Data | Dec 5, 2021

Construction adds 31,000 jobs in November

Gains were in all segments, but the industry will need even more workers as demand accelerates.

Market Data | Dec 5, 2021

Construction spending rebounds in October

Growth in most public and private nonresidential types is offsetting the decline in residential work.

Market Data | Dec 5, 2021

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.