Nonresidential construction spending in New York City is projected to reach $39 billion in 2018, a nearly 66% increase over the previous year. However, spending is also expected to tail off significantly during the following two years, according to a new report, Construction Outlook 2018-2020, released today by the New York Building Congress.

Spending for all types construction in New York City is in its fifth year of growth and could hit a record $61.8 billion this year, 25% more than in 2017. That growth is attributable in part to several large-scale projects. The New York Building Congress forecasts that, despite some anticipated falloff over the next two years, total construction spending through 2020 will total $177 billion.

Nonresidential construction alone—which includes offices, institutional, government buildings, sports and entertainment, and hotels—is forecast to add a record 39 million gross sf this year, followed by 30.4 million sf and 23.4 million sf in 2019 and 2020, respectively. The projected decrease in construction spending for nonresidential buildings over the next two years can be pegged to the completion of several big projects by 2020, such as the 58-story 1,401-ft-tall One Vanderbilt, and three buildings within the $20 billion Hudson Yards redevelopment.

(All this new floor space is coming at a time when New York’s office vacancy rate hovers around 13%, according to the website Optimal Spaces.)

Residential construction spending—which in New York is primarily for multifamily buildings—will total $14 billion in 2018, up 6% from the previous year. Next year, residential construction spending is expected to hit $15 billion, and then recede to $10.6 billion in 2020. (The totals include renovations and alterations.)

Over the three years, 60,000 housing units and 107.2 million gross sf will be added, states the report. The average annual unit count, though, would be off from the 27,898 housing units added to the city in 2017.

The report states that construction employment will show growth for the seventh consecutive year in 2018, and top 150,000 jobs for the second consecutive year. While the Building Congress predicts an employment dip—to 145,600 in 2019 and to 147,700 in 2020—those numbers would still be higher than the average for the last five years.

Related Stories

Market Data | Dec 4, 2019

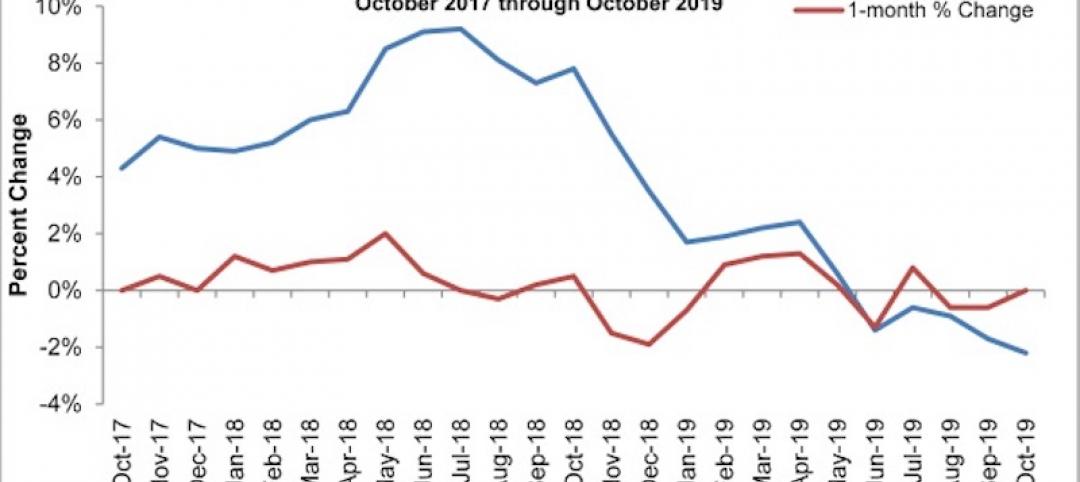

Nonresidential construction spending falls in October

Private nonresidential spending fell 1.2% on a monthly basis and is down 4.3% from October 2018.

Market Data | Nov 25, 2019

Office construction lifts U.S. asking rental rate, but slowing absorption in Q3 raises concerns

12-month net absorption decelerates by one-third from 2018 total.

Market Data | Nov 22, 2019

Architecture Billings Index rebounds after two down months

The Architecture Billings Index (ABI) score in October is 52.0.

Market Data | Nov 14, 2019

Construction input prices unchanged in October

Nonresidential construction input prices fell 0.1% for the month and are down 2.0% compared to the same time last year.

Multifamily Housing | Nov 7, 2019

Multifamily construction market remains strong heading into 2020

Fewer than one in 10 AEC firms doing multifamily work reported a decrease in proposal activity in Q3 2019, according to a PSMJ report.

Market Data | Nov 5, 2019

Construction and real estate industry deals in September 2019 total $21.7bn globally

In terms of number of deals, the sector saw a drop of 4.4% over the last 12-month average.

Market Data | Nov 4, 2019

Nonresidential construction spending rebounds slightly in September

Private nonresidential spending fell 0.3% on a monthly basis and is down 5.7% compared to the same time last year.

Market Data | Nov 1, 2019

GDP growth expands despite reduction in nonresident investment

The annual rate for nonresidential fixed investment in structures declined 15.3% in the third quarter.

Market Data | Oct 24, 2019

Architecture Billings Index downturn moderates as challenging conditions continue

The Architecture Billings Index (ABI) score in September is 49.7.

Market Data | Oct 23, 2019

ABC’s Construction Backlog Indicator rebounds in August

The primary issue for most contractors is not a lack of demand, but an ongoing and worsening shortage of skilled workers available to meet contractual requirements.