Transwestern’s second-quarter national office market report highlights continued improvement in the sector thanks in large part to a strong jobs market with remarkably low overall unemployment of 3.9%, and a 1.6% annual growth rate in office-using employment.

For the second quarter, office absorption totaled 18.8 million square feet, vacancy remained stable at 9.6%, and average asking rents increased by 3.4% annually to $25.71 per square foot.

“As more individuals return to the workforce citing real wage growth, further tightening in the core metrics is anticipated through the balance of the year,” said Stuart Showers, Research Director in Houston.

The rise in rental rates marks the 21st consecutive quarterly increase, with Minneapolis; Charlotte, North Carolina; Columbus, Ohio; San Antonio and Austin, Texas leading the nation in year-over-year rent growth. San Francisco edged out New York for the highest asking rates in the country at $74.40 per square foot.

“Despite only 4 million square feet currently under construction in San Francisco versus more than 14 million square feet in New York, San Francisco is increasing total inventory by a higher percentage, which could drive asking rates even higher as new product comes online,” said Ryan Tharp, Research Director in Dallas. “Additionally, existing tariffs on steel and aluminum are likely to drive up construction costs, and landlords may need to bump up rental rates to compensate.”

Worth noting is that while national quarterly absorption remained positive, the pace of absorption is slowing as quarterly totals are approximately 20% below three- and five-year quarterly averages. Overall, 34 of the 49 Transwestern reporting markets registered positive absorption in the second quarter, underscoring the strength of the sector.

Download the national office market report at: http://twurls.com/2q18-us-offi

Related Stories

Market Data | Dec 4, 2019

Nonresidential construction spending falls in October

Private nonresidential spending fell 1.2% on a monthly basis and is down 4.3% from October 2018.

Market Data | Nov 25, 2019

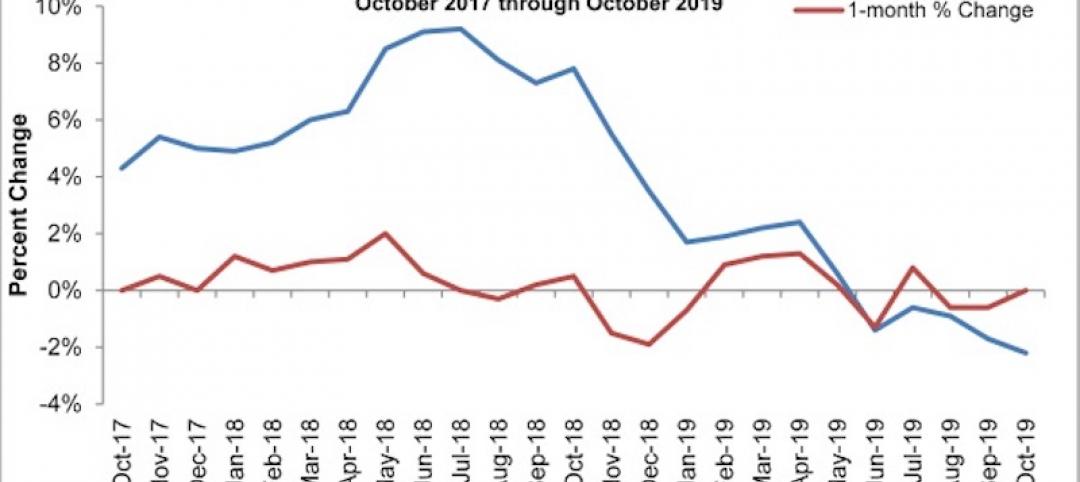

Office construction lifts U.S. asking rental rate, but slowing absorption in Q3 raises concerns

12-month net absorption decelerates by one-third from 2018 total.

Market Data | Nov 22, 2019

Architecture Billings Index rebounds after two down months

The Architecture Billings Index (ABI) score in October is 52.0.

Market Data | Nov 14, 2019

Construction input prices unchanged in October

Nonresidential construction input prices fell 0.1% for the month and are down 2.0% compared to the same time last year.

Multifamily Housing | Nov 7, 2019

Multifamily construction market remains strong heading into 2020

Fewer than one in 10 AEC firms doing multifamily work reported a decrease in proposal activity in Q3 2019, according to a PSMJ report.

Market Data | Nov 5, 2019

Construction and real estate industry deals in September 2019 total $21.7bn globally

In terms of number of deals, the sector saw a drop of 4.4% over the last 12-month average.

Market Data | Nov 4, 2019

Nonresidential construction spending rebounds slightly in September

Private nonresidential spending fell 0.3% on a monthly basis and is down 5.7% compared to the same time last year.

Market Data | Nov 1, 2019

GDP growth expands despite reduction in nonresident investment

The annual rate for nonresidential fixed investment in structures declined 15.3% in the third quarter.

Market Data | Oct 24, 2019

Architecture Billings Index downturn moderates as challenging conditions continue

The Architecture Billings Index (ABI) score in September is 49.7.

Market Data | Oct 23, 2019

ABC’s Construction Backlog Indicator rebounds in August

The primary issue for most contractors is not a lack of demand, but an ongoing and worsening shortage of skilled workers available to meet contractual requirements.