Entering the second quarter of 2022, FMI expects construction spending to end 2022 up 7% compared to up 8% in 2021. But that growth will be offset by inflation, supply chain snarls, a shortage of workers, project delays and economic turmoil caused by international events such as the Russia-Ukraine war, according to FMI's 2022 North American Engineering and Construction Outlook Second Quarter Edition.

Key highlights of the report include:

- Strong investment in residential and manufacturing will drive industry spending through 2022.

- Due to expected increases in infrastructure funding later this year, several nonbuilding segments, including highway and street, sewage and waste disposal and water supply, are all anticipated to realize growth rates of more than 5% in 2022.

- Year-end 2022 growth will be tempered by ongoing spending declines across various nonresidential building segments, including lodging, office, educational, religious, public safety and amusement and recreation.

- Commercial, health care, communication, power and conservation and development are all expected to end the year with low growth, roughly in line with the historical rate of inflation, between 0% and 4%, and are therefore considered stable.

Download the free PDF report (short registration required).

Related Stories

Market Data | Dec 15, 2021

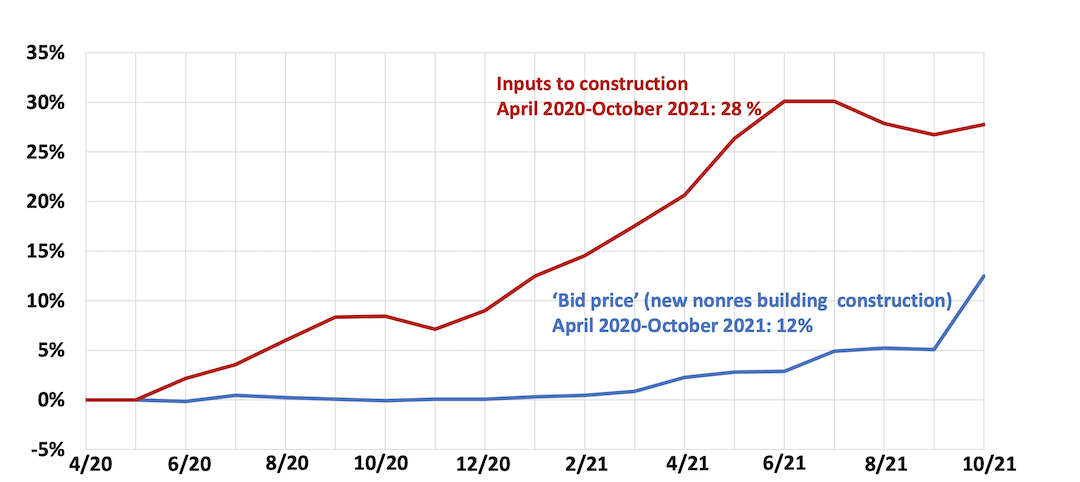

Widespread steep increases in materials costs in November outrun prices for construction projects

Construction officials say efforts to address supply chain challenges have been insufficient.

Market Data | Dec 15, 2021

Demand for design services continues to grow

Changing conditions could be on the horizon.

Market Data | Dec 5, 2021

Construction adds 31,000 jobs in November

Gains were in all segments, but the industry will need even more workers as demand accelerates.

Market Data | Dec 5, 2021

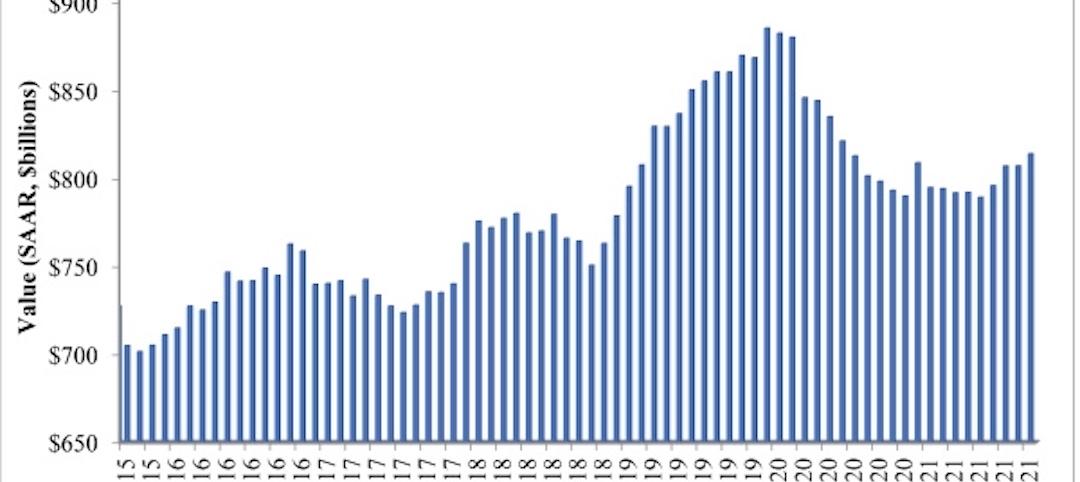

Construction spending rebounds in October

Growth in most public and private nonresidential types is offsetting the decline in residential work.

Market Data | Dec 5, 2021

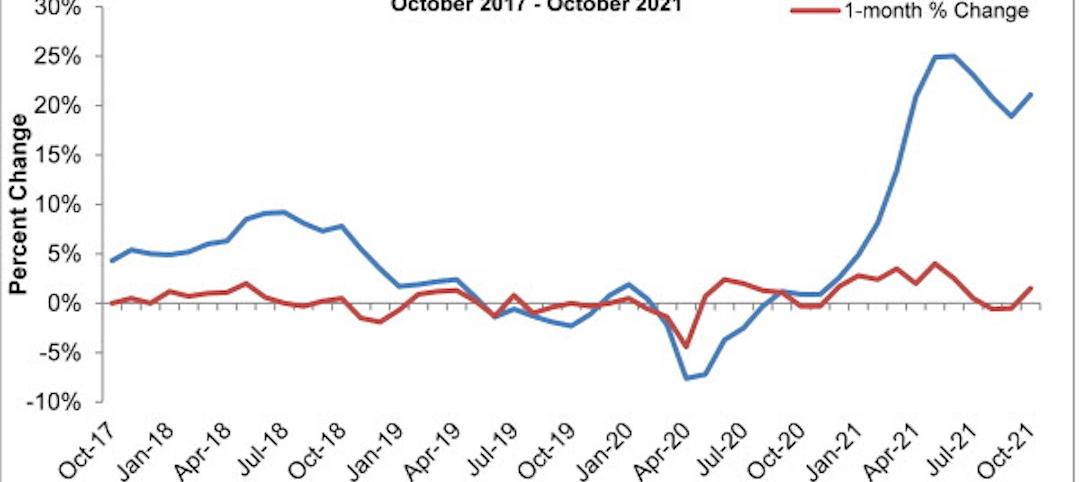

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.