U.S. construction industry leaders remained upbeat regarding nonresidential construction’s near-term prospects in May 2019, according to the Construction Confidence Index released today by Associated Builders and Contractors.

While contractors were slightly less upbeat regarding profit margins and staffing levels compared to April, all three principal components measured by the survey—sales, profit margins and staffing levels—remain well above the diffusion index threshold of 50 in May. Nearly 73% of contractors expect sales to rise during the next six months and 68% expect staffing levels to increase further.

- The CCI for sales expectations increased from 68.4 to 70.0 in May.

- The CCI for profit margin expectations fell slightly from 63.0 to 62.8.

- The CCI for staffing levels fell from 67.4 to 66.8.

“While there continues to be considerable chatter regarding a slowing economy, the need for federal rate cuts and the damaging effects of ongoing trade disputes involving the United States, China, the European Union and India, among others, nonresidential firm leaders continue to expect further construction spending growth,” said ABC Chief Economist Anirban Basu. “Recent data regarding job growth and consumer spending indicate that any economic slowing to date has been mild and that the expansion is set to endure for the next few quarters.

“While profit margin expectations and staffing levels measures declined slightly in May, they remained well above the threshold level of 50,” said Basu. “More importantly, these CCI measures likely declined due to economic strength rather than weakness. Firms continue to scramble for talent in the context of an economy offering more job openings than jobseekers. As a result, staffing levels cannot rise rapidly even in the context of elevated demand for workers, and profit margins are negatively impacted by the accompanying rapid rise in compensation costs. However, far more industry leaders expect profit margins to rise than decline.

“As we reach the longest economic expansion in American history, recent construction spending data indicate that much of the momentum is coming from public projects,” said Basu. “Years of growth have helped to stabilize state and local government finances, resulting in more money available to fund transportation, water, public safety and other projects. While spending in certain private segments has been expanding less rapidly of late, this nascent weakness has been more than fully countervailed by the strength of investment in infrastructure.”

CCI is a diffusion index. Readings above 50 indicate growth, while readings below 50 are unfavorable.

.jpg%3Fver%3D2019-07-18-104421-307&I=20190718150919.0000053f0b67%40mail6-60-usnbn1&X=MHwxMDQ2NzU4OjVkMzA3OTVhZDdkNzRjY2IwYWNjM2ViYzs%3D&S=cVBNKOEoq6MUK-bwGgOO7KJ8uiyNh3t6BAKLaMNS0L0)

Related Stories

Market Data | Dec 17, 2021

Construction jobs exceed pre-pandemic level in 18 states and D.C.

Firms struggle to find qualified workers to keep up with demand.

Market Data | Dec 15, 2021

Widespread steep increases in materials costs in November outrun prices for construction projects

Construction officials say efforts to address supply chain challenges have been insufficient.

Market Data | Dec 15, 2021

Demand for design services continues to grow

Changing conditions could be on the horizon.

Market Data | Dec 5, 2021

Construction adds 31,000 jobs in November

Gains were in all segments, but the industry will need even more workers as demand accelerates.

Market Data | Dec 5, 2021

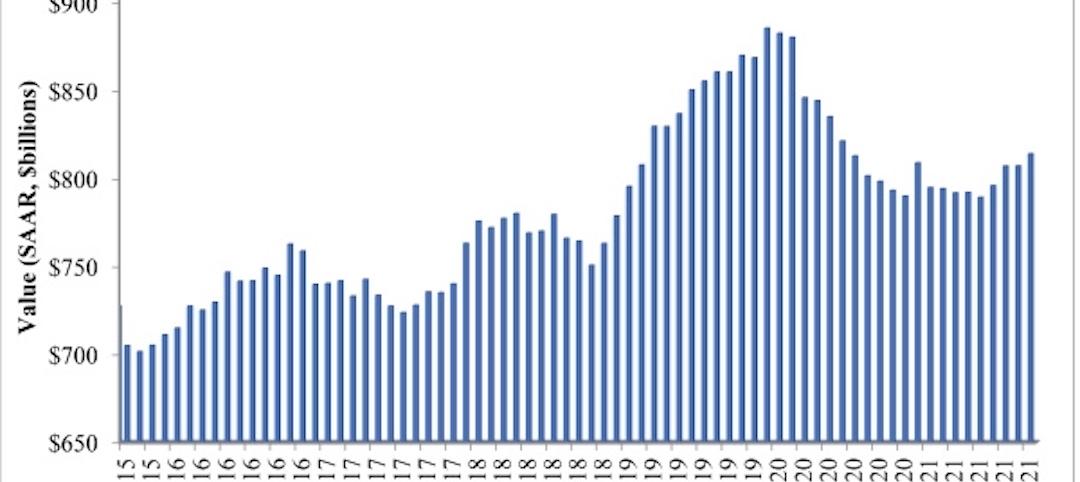

Construction spending rebounds in October

Growth in most public and private nonresidential types is offsetting the decline in residential work.

Market Data | Dec 5, 2021

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

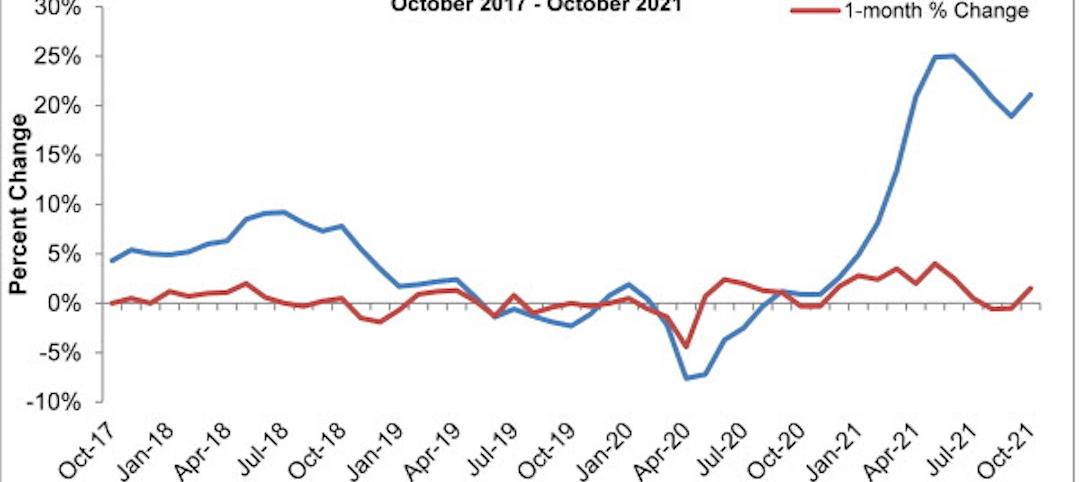

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

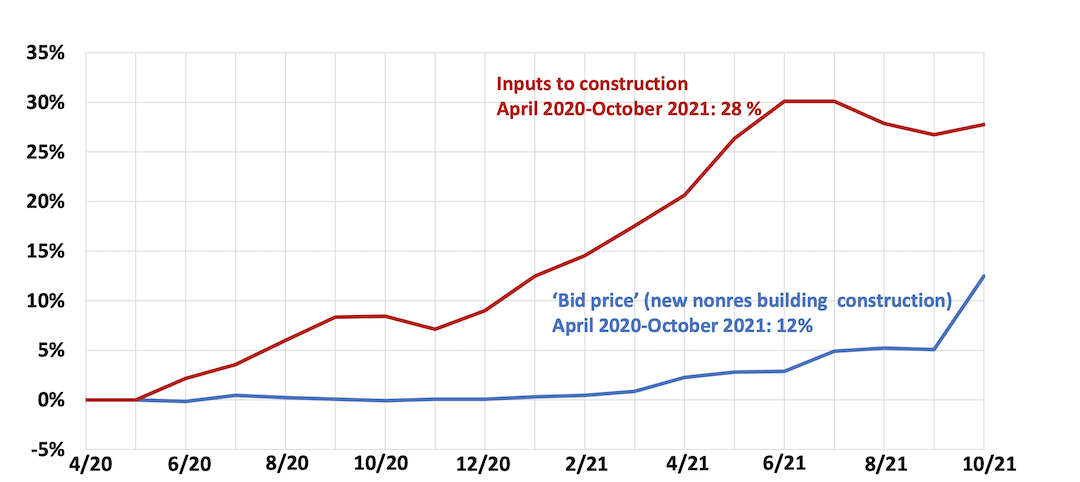

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.