Construction industry leaders remained upbeat with respect to nonresidential construction prospects in March 2019, according to the latest Construction Confidence Index released today by Associated Builders and Contractors.

All three principal components measured by the survey—sales, profit margins and staffing levels— remained well above the diffusion index threshold of 50, signaling ongoing expansion in construction activity. While contractors are slightly less upbeat regarding profit margins and staffing levels than in February, more than 70% of contractors expect to increase staffing levels over the next six months, a reflection of continued elevated demand for construction services. Despite rising wage pressures, more than 56% of survey respondents anticipate rising profit margins, an indication that users of construction services remain willing to pay more to get projects delivered.

- The CCI for sales expectations increased from 69.4 to 69.6 in March.

- The CCI for profit margin expectations fell from 63.3 to 61.8.

- The CCI for staffing levels fell from 68.5 to 67.8.

“Last year, the U.S. economy grew 2.9%, and it expanded an additional 3.2% during the first quarter of 2019,” said ABC Chief Economist Anirban Basu. “All of this is consistent with the notion that demand for nonresidential construction services will remain elevated for the foreseeable future. The CCI findings are also consistent with ABC’s latest Construction Backlog Indicator report, which revealed that many contractors have a growing number of projects in their pipeline.

“A major source of influence on the data is the reemergence of public construction spending,” said Basu. “With nearly 10 years of economic expansion complete, many state and local governments are experiencing their best fiscal health in years, resulting in more funds to invest in roads, transit systems, schools, fire stations and police stations. The combination of spending growth in certain private construction categories and rising infrastructure outlays will keep the average American nonresidential contractor scrambling to retain and recruit workers, especially in the context of a national rate of unemployment effectively at a 50-year low.

“It should be noted that the most recent CCI survey was completed prior to the turmoil associated with the trade dispute between the United States and China, which may impact contractor confidence,” said Basu. “While global investors have exhibited concern, most construction activity involves U.S.-based enterprises providing services to U.S.-based customers, minimizing unease. That said, the imposition of tariffs has the potential to raise costs of equipment and other inputs, which could at least conceivably impact profit margins. Moreover, market turmoil can truncate the availability of financing to prospective construction projects.”

CCI is a diffusion index. Readings above 50 indicate growth, while readings below 50 are unfavorable.

ABC Construction Confidence Index, March 2019

Related Stories

Market Data | Sep 6, 2023

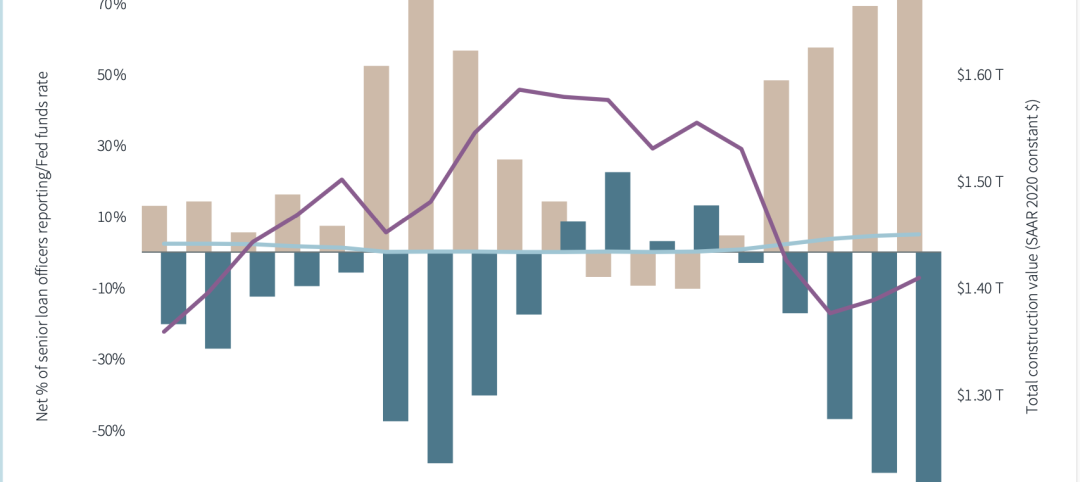

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Apartments | Aug 22, 2023

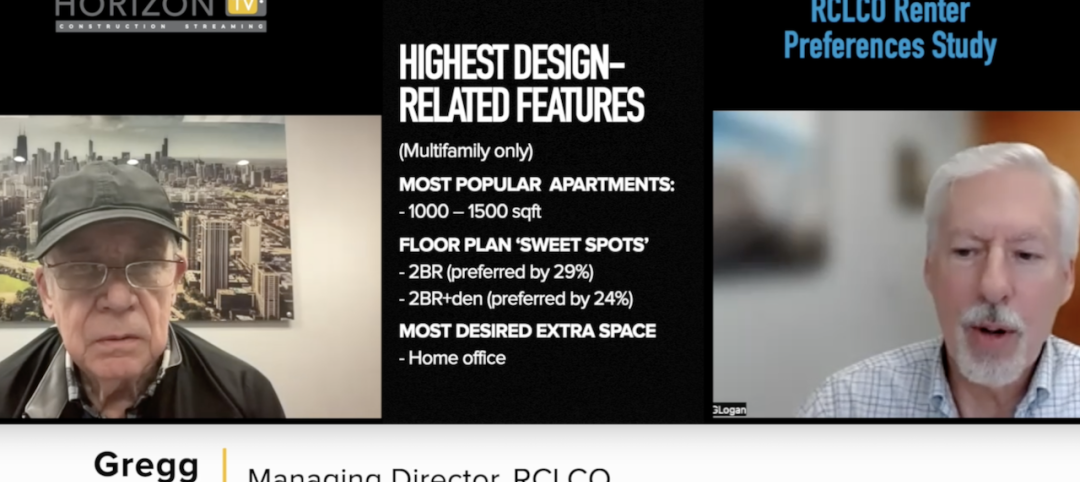

Key takeaways from RCLCO's 2023 apartment renter preferences study

Gregg Logan, Managing Director of real estate consulting firm RCLCO, reveals the highlights of RCLCO's new research study, “2023 Rental Consumer Preferences Report.” Logan speaks with BD+C's Robert Cassidy.

Market Data | Aug 18, 2023

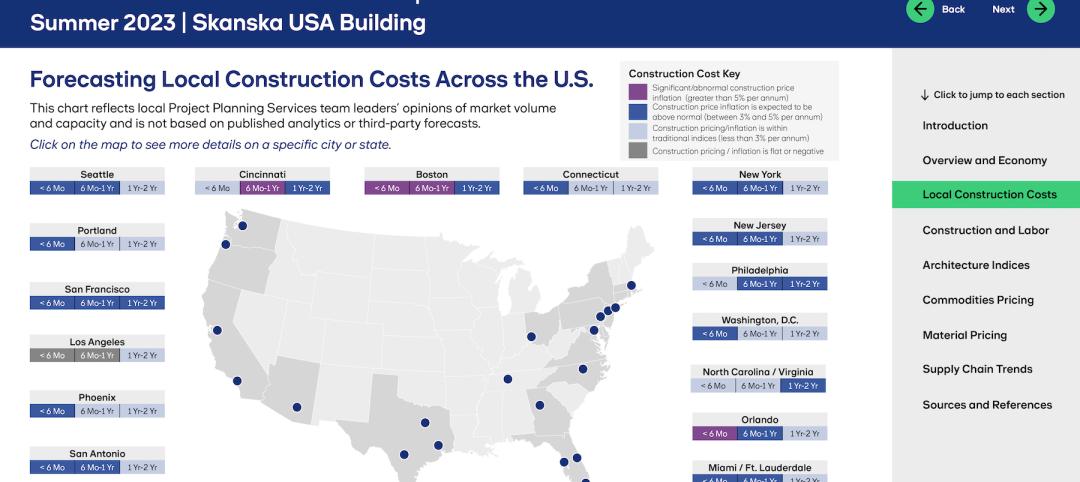

Construction soldiers on, despite rising materials and labor costs

Quarterly analyses from Skanska, Mortenson, and Gordian show nonresidential building still subject to materials and labor volatility, and regional disparities.