U.S. architecture firms have experienced a near complete recovery from the Great Recession, which has allowed firm leaders to reinvest profits back into their businesses. These findings, along with an in depth look at topics such as firm billings, staffing, and international work, are covered in The Business of Architecture: 2016 Firm Survey Report.

Key highlights include:

- Net billings at architecture firms were $28.5 billion at the peak of the market in 2008 and had nearly recovered to $28.4 billion by 2015.

- Percentage of firms reporting a financial loss declined sharply in recent years from more than 20% in 2011 to fewer than 10% by 2015.

- Growing profitability has allowed firms to increase their marketing activities and expand into new geographical areas and building types to diversity their design portfolios.

- Renovations made up a large portion of design work with 45% of building design billings coming from work on existing facilities, including 30% from additions to buildings, and the remaining from historic preservation projects.

- Billings in the residential sector topped $7 billion, more than 30% over 2013 levels.

- Modest gains in diversity of profession with women now comprising 31% of architecture staff (up from 28% in 2013) and minorities making up 21% of staff (up from 20% in 2013).

- Use of Building Information Modeling (BIM) software has become standard at larger firms with 96% of firms with 50 or more employees report using it for billable work (compared to 72% of mid-sized firms and 28% of small firms).

- Newer technologies including 3D printing and 4D/5D modeling are reported being used at only 11% and 8% of firms respectively.

- Energy modeling currently has a low adoption rate with 13% of firms using it for billable work, although this share jumps to 59% for large firms.

“In the coming years we expect firms will be adding technological dimensions to their design work through greater utilization of cloud computing, 3D printing and the use of virtual reality software. This should help further efficiencies, minimize waste and project delivery delays, and lead to increased bottom line outcomes for their clients,” says AIA senior director of research, Michele Russo in a press release.

Related Stories

Market Data | Aug 10, 2018

Construction material prices inch down in July

Nonresidential construction input prices increased fell 0.3% in July but are up 9.6% year over year.

Market Data | Aug 9, 2018

Projections reveal nonresidential construction spending to grow

AIA releases latest Consensus Construction Forecast.

Market Data | Aug 7, 2018

New supply's impact illustrated in Yardi Matrix national self storage report for July

The metro with the most units under construction and planned as a percent of existing inventory in mid-July was Nashville, Tenn.

Market Data | Aug 3, 2018

U.S. multifamily rents reach new heights in July

Favorable economic conditions produce a sunny summer for the apartment sector.

Market Data | Aug 2, 2018

Nonresidential construction spending dips in June

“The hope is that June’s construction spending setback is merely a statistical aberration,” said ABC Chief Economist Anirban Basu.

Market Data | Aug 1, 2018

U.S. hotel construction pipeline continues moderate growth year-over-year

The hotel construction pipeline has been growing moderately and incrementally each quarter.

Market Data | Jul 30, 2018

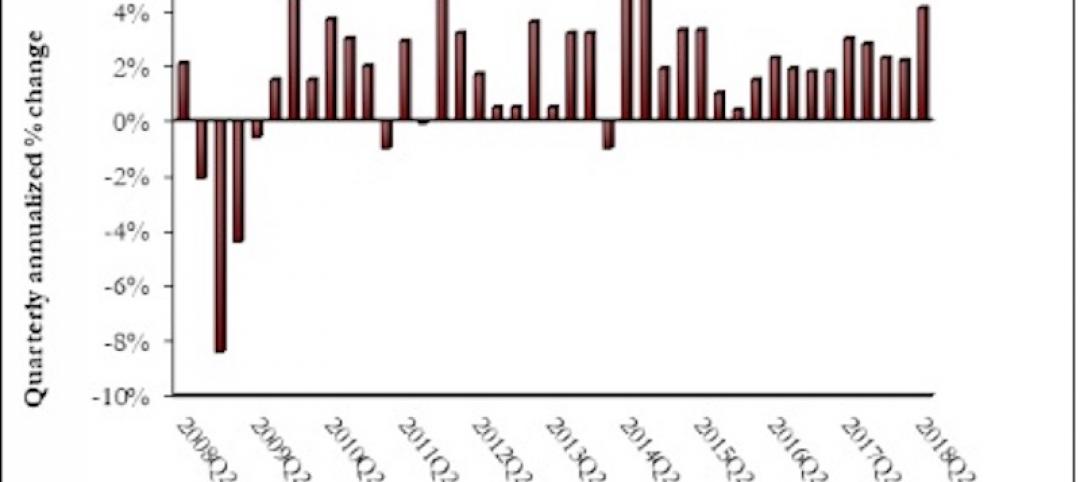

Nonresidential fixed investment surges in second quarter

Nonresidential fixed investment represented an especially important element of second quarter strength in the advance estimate.

Market Data | Jul 11, 2018

Construction material prices increase steadily in June

June represents the latest month associated with rapidly rising construction input prices.

Market Data | Jun 26, 2018

Yardi Matrix examines potential regional multifamily supply overload

Outsize development activity in some major metros could increase vacancy rates and stagnate rent growth.

Market Data | Jun 22, 2018

Multifamily market remains healthy – Can it be sustained?

New report says strong economic fundamentals outweigh headwinds.