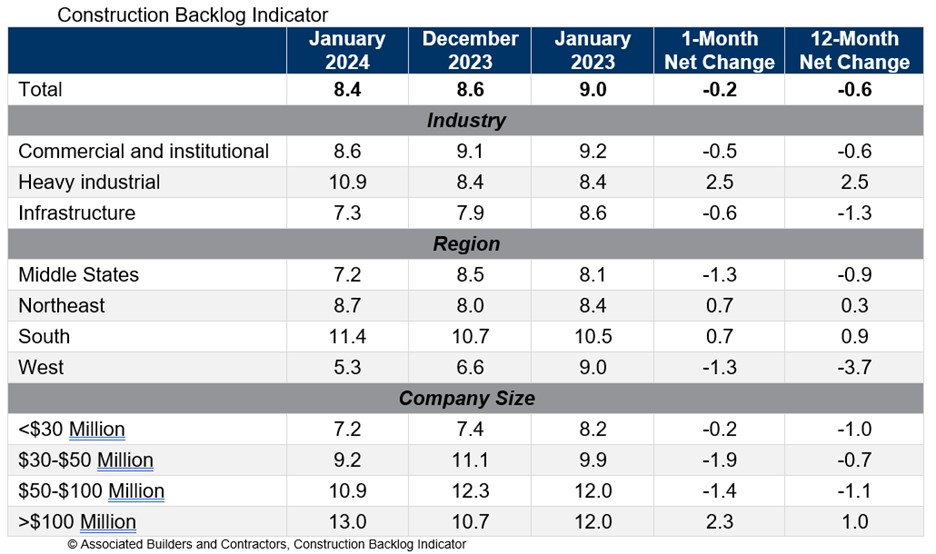

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.4 months in January, according to an ABC member survey conducted from Jan. 22 to Feb. 4. The reading is down 0.6 months from January 2023.

Backlog increased to 10.9 months in the heavy industrial category, the highest reading on record for that category, and is 2.5 months higher than in January 2023. Backlog is down on a year-over-year basis in the commercial/institutional and infrastructure categories.

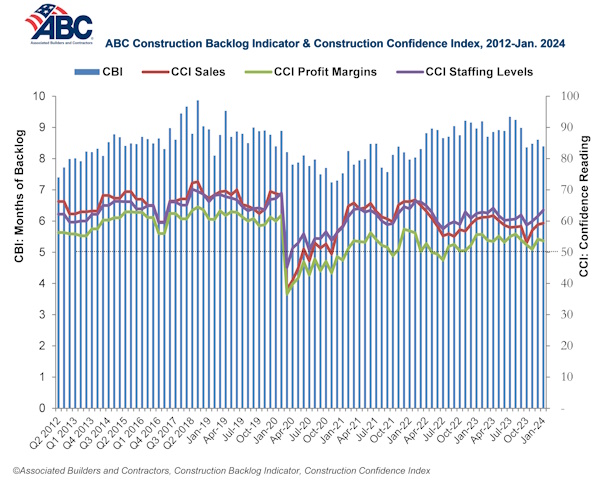

ABC’s Construction Confidence Index readings for sales and staffing levels increased in January, while the reading for profit margins declined. All three readings remain above the threshold of 50, indicating expectations for growth over the next six months.

“As predicted, performance in the nonresidential construction sector is becoming more disparate across segments,” said ABC Chief Economist Anirban Basu. “For much of the pandemic recovery period, contractors in virtually all segments were indicating stable to rising backlog. That remains the case for contractors most exposed to the nation’s industrial production. Reshoring and near-shoring continue to drive construction spending.

“In other categories, however, including those most interest rate-sensitive, activity appears to be slowing,” said Basu. “Developer financing has become both more expensive and more difficult to obtain over roughly the past year, in part because of rising office vacancy in many markets. That helps to explain declining backlog in the commercial category. The decline in infrastructure-related backlog may be due only to seasonality, however. There is every reason to believe that contractors specializing in public works will have a very busy year.”

Related Stories

Healthcare Facilities | Feb 1, 2018

Early supplier engagement provides exceptional project outcomes

Efficient supply chains enable companies to be more competitive in the marketplace.

Industry Research | Jan 30, 2018

AIA’s Kermit Baker: Five signs of an impending upturn in construction spending

Tax reform implications and rebuilding from natural disasters are among the reasons AIA’s Chief Economist is optimistic for 2018 and 2019.

Market Data | Jan 30, 2018

AIA Consensus Forecast: 4.0% growth for nonresidential construction spending in 2018

The commercial office and retail sectors will lead the way in 2018, with a strong bounce back for education and healthcare.

Architects | Jan 29, 2018

14 marketing resolutions AEC firms should make in 2018

As we close out the first month of the New Year, AEC firms have made (and are still making) plans for where and how to spend their marketing time and budgets in 2018.

AEC Tech | Jan 29, 2018

thyssenkrupp tests self-driving robot for ‘last mile’ delivery of elevator parts

“With driverless delivery robots, we could fill a gap and get spare parts from our warehouses to the jobsite faster,” said thyssenkrupp SVP Ivo Siebers.

Contractors | Jan 26, 2018

6 regional construction trends for 2018

2018 should be a good year for construction but there are at least 4 things that can influence costs.

K-12 Schools | Jan 25, 2018

Cost estimating for K-12 school projects: An invaluable tool for budget management

Clients want to be able to track costs at every stage of a project, and cost estimates (current and life cycle) are valuable planning and design tools, writes LS3P's Ginny Magrath, AIA.

AEC Tech | Jan 25, 2018

Four high-tech solutions to mitigate theft on the jobsite

Geo-fencing and drone surveillance are among the tech solutions for protecting jobsites from asset loss.

Multifamily Housing | Jan 24, 2018

Apartment rent rates jump 2.5% in 2017, led by small and mid-sized markets

The average price for one-bedroom units increased the most.

Hotel Facilities | Jan 24, 2018

U.S. hotel markets with the largest construction pipelines

Dallas, Houston, and New York lead the way, with more than 460 hotel projects in the works.