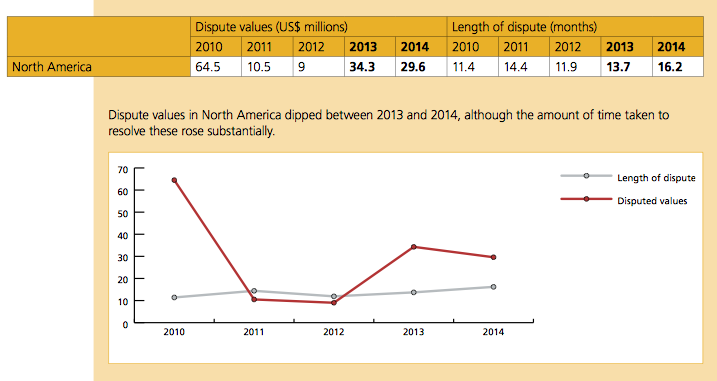

For the second consecutive year, the leading cause of construction contract disputes in North America was errors and/or omissions in contract documents. And while the value of disputes fell by nearly 14% in 2014, the time it took to resolve them lengthened substantially last year.

These are some of the key findings in the “Global Construction Disputes Report 2015,” the fifth such annual report produced by Arcadis, a leading global natural and built asset design and consultancy firm. Its data are based on contract disputes handled by Arcadis’ Construction Claims Consulting teams in North America, Europe, the UK, the Middle East, and Asia.

(Arcadis could not provide statistics on the total value of disputes. But last year it served as a claims consultant on approximately 40 disputes with values up to $100 million last year.)

Globally, the report found an increase in the value and length of disputes, with the most common cause being a failure to properly administer the contract. “This is both a revealing and concerning statistic,” observes Mike Allen, Arcadis’ Global Leader of Contract Solutions. “It raises myriad questions as to how projects and programs are briefed, scoped, [and] structured,” as well as questions about resourcing, training, and contracting environment itself.

The transportation sector accounted for 31% of global contract disputes. And despite the presumed advantages of joint ventures, one in three still ends up in a contract dispute, although that number dips to less than one in five (19.8%) in North America.

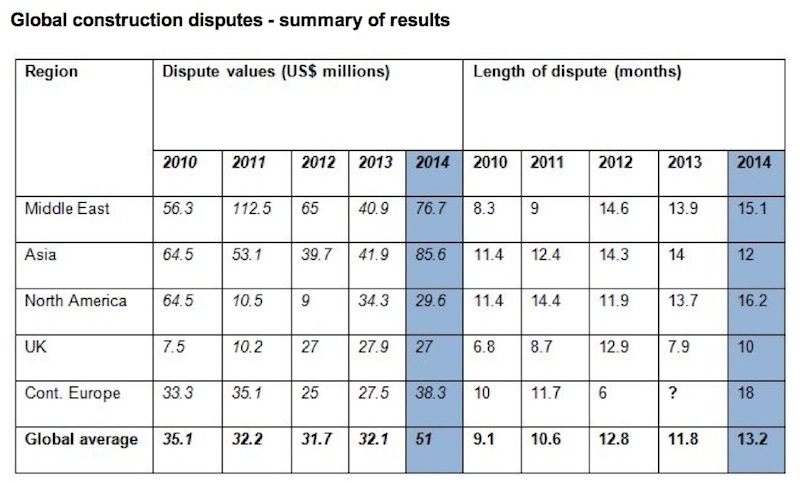

Worldwide, the average value of disputes increased last year to $51 million, from $32.1 million in 2013. The highest average was in Asia, where dispute values more than doubled to $85.6 million. Arcadis attributed the jump primarily to the region’s growth, the complexity of its construction projects, and the rise in joint ventures.

Dispute values in the Middle East rose to $76.7 million, from $40.9 million in 2013. In the UK, dispute values dipped slightly to $27 million.

The average time taken to resolve disputes globally rose to 13.2 months, up from just under 12 months in 2013. All areas of the world saw their resolution processes extend, with the exception of Asia where the average dispute length took two months less than it did the year before.

In North America, the length of disputes last year increased by more than 18% to 16.2 months. On the other hand, dispute values dipped by nearly 14% to $29.6 million, and there was evident willingness on behalf of contractual parties “to try and try again to arrive at a settlement” and avoid the inevitably escalating costs associated with formal litigation and negative publicity, said Roy Cooper, Arcadis’ Vice President and Head of Contract Solutions in North America.

For the second year running, the most common cause of disputes in North America during 2014 was errors and/or omissions in the contract documents. Differing site conditions came in second, while a failure to understand or comply with contractual obligations on the part of an employer, contractor or subcontractor was the third most commonly cited reason for a dispute.

With North America’s crumbling infrastructure system in need of a significant overhaul, Cooper sees the construction industry moving towards a program of interconnected projects, rather than discrete projects. But big programs can come with bigger risks, so “failure and high visibility disputes are not an option,” he said. “Owners have turned to alternate project delivery, increased project controls and early intervention to mitigate disputes to help manage that risk.”

The three most common methods of Alternate Dispute Resolution in the U.S. were party-to-party negotiation, mediation, and arbitration.

Still, Arcadis predicts that the number of projects going into dispute would to rise this year globally, with projects accepted for lower margins during economic downturns and labor shortages in some markets likely to prove the catalysts for disputes.

Related Stories

Giants 400 | Sep 15, 2015

HOTEL SECTOR GIANTS: Gensler, AECOM, Turner among nation's largest hotel sector AEC firms

BD+C's rankings of the nation's largest hotel sector design and construction firms, as reported in the 2015 Giants 300 Report.

Contractors | Sep 14, 2015

Gilbane report: Nonres building on brink of ‘breakout’ spending year

Total construction spending is on pace to achieve double-digit growth in 2015, and a strong single-digit increase next year. But finding labor will be tough.

Giants 400 | Sep 10, 2015

INDUSTRIAL SECTOR GIANTS: Stantec, Turner, Jacobs among top industrial AEC firms

BD+C's rankings of the nation's largest industrial sector design and construction firms, as reported in the 2015 Giants 300 Report

Giants 400 | Sep 10, 2015

MILITARY SECTOR GIANTS: Clark Group, HDR, Fluor top rankings of nation's largest military sector AEC firms

BD+C's rankings of the nation's largest military sector design and construction firms, as reported in the 2015 Giants 300 Report

Contractors | Sep 9, 2015

ABC: Construction activity increases as backlog edges higher

The backlog indicator is up 1% to 8.5 months during the second quarter of 2015.

Giants 400 | Sep 8, 2015

RETAIL SECTOR GIANTS: Callison RTKL, PCL Construction, Jacobs among top retail sector AEC firms

BD+C's rankings of the nation's largest retail sector design and construction firms, as reported in the 2015 Giants 300 Report

BIM and Information Technology | Sep 7, 2015

The power of data: How AEC firms and owners are using analytics to transform design and construction

Case’s bldgs = data conference highlighted how collecting data about personal activities can inform design and extend the power of BIM/VDC.

Industrial Facilities | Sep 3, 2015

DATA CENTER SECTOR GIANTS: Fluor, Gensler, Holder Construction among top data center AEC firms

BD+C's rankings of the nation's largest data center sector design and construction firms, as reported in the 2015 Giants 300 Report

Airports | Aug 31, 2015

Surveys gauge users’ satisfaction with airports

Several surveys gauge passenger satisfaction with airports, as flyers and airlines weigh in on technology, security, and renovations.

Airports | Aug 31, 2015

Small and regional airports in a dogfight for survival

Small and regional airports are in a dogfight for survival. Airlines have either cut routes to non-hub markets, or don’t provide enough seating capacity to meet demand.