The new Trump Administration’s aggressive policies, particularly on international trade and immigration reform, could, if executed as planned, “greatly affect” how America’s construction industry does business this year and beyond.

In its Q4 2016 Construction Outlook, which it released earlier this week, JLL also continued to see construction labor as a “pain point” for the industry that will cause wages to rise and impact project timelines and budgets. And materials costs, which for the most part stabilized in the latter months of 2016, should hold steady if, as expected, construction activity slows this year.

Twenty-sixteen was a banner year for construction spending. Led by the hotel and office sectors, spending increased over the previous year by 4.5% to $1.2 trillion. That rate of growth was nearly triple the GDP inflation rate.

Nationally, the construction and contractor backlog in Q4 2016 stood at 8.7 months of future work across all sectors, up 2.2 percent from the fourth quarter 2015 and tracking closely with national trends. The Midwest in particular enjoyed sizable year-over-year growth that quarter, while work in the South remains steady. The Northeast and West regions continued to slip, each well below 2015 levels.

Not surprisingly, construction costs are rising faster in metros where construction activity has been robust, but also where labor is in shorter supply. Image: JLL Research

Building costs rose nationally by a modest 2.7%, with nearly half of that increase occurring in the fourth quarter, spurred by strong residential construction that drove demand, and uncertainly surrounding the effects of the Trump presidency.

JLL doesn’t expect the manifestations of policy decisions coming out of Washington to intervene on the construction industry until later this year. But JLL’s forecast strikes a cautionary pose about the prospects of “voided international trade deals and new import tariffs [that] could drive up materials costs faster.”

And at a time when construction unemployment continues to fall—last week, AGC America reported that from January 2016 to January 2017 construction employment rose in 39 states and in 216 of 358 metro areas—immigration reform “could shrink the skilled labor supply and spur further wage increases,” says JLL’s report. Large-scale infrastructure projects will create a premium on materials and workforce in specific markets such as Oakland and San Francisco, Chicago, and New York.

Inflation in materials costs is harder to gauge when trade agreements are in flux. The largest price swings in 4Q 2016 were seen on the cement and lumber fronts: cement costs were down 4.7% compared to the same time last year, while lumber was priced 9%-plus higher. Steel, on the other hand, maintained negligible price changes, not even breaking one-tenth of a percentage point over third-quarter prices.

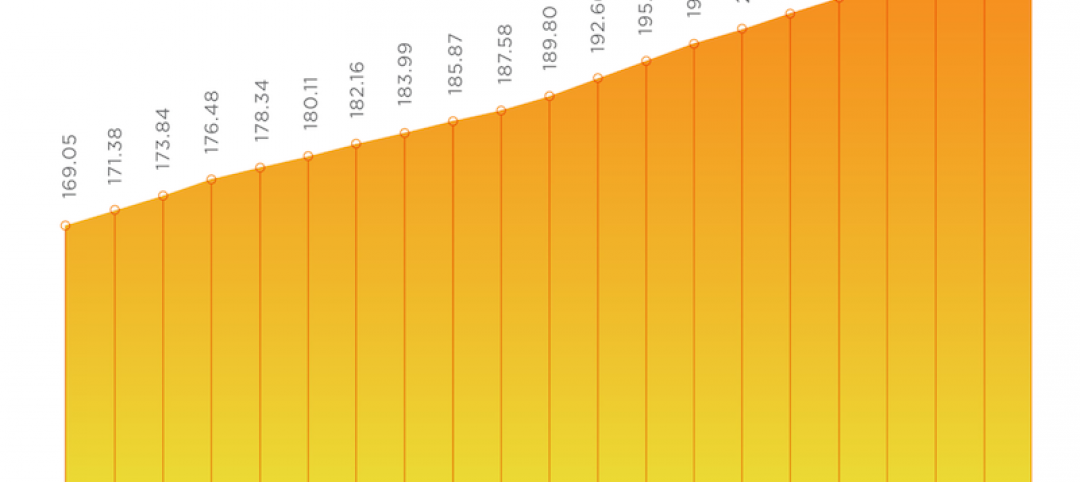

One barometer worth keeping an eye on is the IHS Markit PEG Engineering and Construction Cost Index, which tracks procurement activity among engineering and construction firms. In March, that Index registered its fifth consecutive month of rising prices.

Eight of 12 materials/equipment categories tracked showed rising prices in March. And the six-month expectation index stayed positive, although materials and equipment prices are projected to rise at a slower pace than subcontractor labor.

Related Stories

Market Data | Jan 19, 2021

Architecture Billings continue to lose ground

The pace of decline during December accelerated from November.

Market Data | Jan 19, 2021

2021 construction forecast: Nonresidential building spending will drop 5.7%, bounce back in 2022

Healthcare and public safety are the only nonresidential construction sectors that will see growth in spending in 2021, according to AIA's 2021 Consensus Construction Forecast.

Market Data | Jan 13, 2021

Atlanta, Dallas seen as most favorable U.S. markets for commercial development in 2021, CBRE analysis finds

U.S. construction activity is expected to bounce back in 2021, after a slowdown in 2020 due to challenges brought by COVID-19.

Market Data | Jan 13, 2021

Nonres construction could be in for a long recovery period

Rider Levett Bucknall’s latest cost report singles out unemployment and infrastructure spending as barometers.

Market Data | Jan 13, 2021

Contractor optimism improves as ABC’s Construction Backlog inches up in December

ABC’s Construction Confidence Index readings for sales, profit margins, and staffing levels increased in December.

Market Data | Jan 11, 2021

Turner Construction Company launches SourceBlue Brand

SourceBlue draws upon 20 years of supply chain management experience in the construction industry.

Market Data | Jan 8, 2021

Construction sector adds 51,000 jobs in December

Gains are likely temporary as new industry survey finds widespread pessimism for 2021.

Market Data | Jan 7, 2021

Few construction firms will add workers in 2021 as industry struggles with declining demand, growing number of project delays and cancellations

New industry outlook finds most contractors expect demand for many categories of construction to decline.

Market Data | Jan 5, 2021

Barely one-third of metros add construction jobs in latest 12 months

Dwindling list of project starts forces contractors to lay off workers.

Market Data | Jan 4, 2021

Nonresidential construction spending shrinks further in November

Many commercial projects languish, even while homebuilding soars.