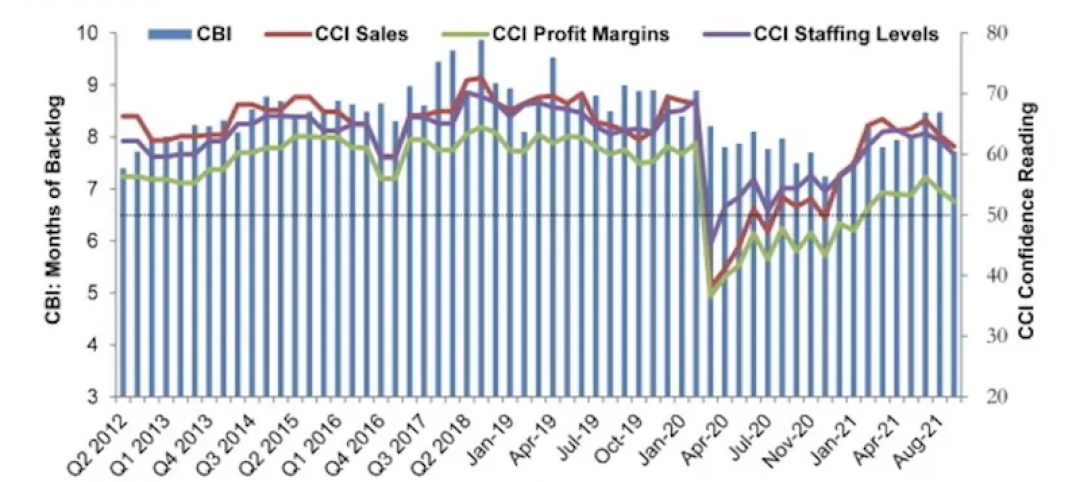

Associated Builders and Contractors (ABC) reports that its Construction Backlog Indicator (CBI) contracted to 8.8 months during the first quarter of 2018, down 9% from the prior quarter. CBI is down 2% on a year-over-year basis.

“The Construction Backlog Indicator hit an all-time high during the fourth quarter of 2017,” said ABC Chief Economist Anirban Basu. “A number of factors pushed backlog lower during the first quarter of 2018, including an extensive winter. Only one region has experienced a decline in backlog on a year-over-year basis: the Middle States, which encompasses the Upper Midwest. There also was a significant uptick in survey participation during the first quarter, which may have helped shape the result. In sum, average backlog remains lofty by historic standards.

“Given improved weather and normal seasonal factors, it is likely that backlog will bounce back during the second quarter. However, the level of improvement may be undermined by a combination of worker shortages and rapidly rising construction materials prices. Despite recent increases in the costs of delivering construction services due to rising human capital and materials costs, there is scant evidence of a decline in demand for construction services,” said Basu.

Highlights by Region

— Backlog in the South fell 8% during the first quarter, but remains 2.9% higher on a year-over-year basis. Large metropolitan areas such as Tampa, Fla., Atlanta, Dallas and Austin, Texas, continue to generate significant construction activity. Expect backlog to remain lengthy as communities impacted by last year’s storms continue to rebuild.

— Backlog in the Northeast fell after expanding for five consecutive quarters. Large cities along the northeast corridor continue to attract commercial investment, including the suburbs of Baltimore. Despite the first quarter decline in backlog, the region’s reading remains elevated by historical standards.

— Backlog in the Middle States is down 12.6% for the quarter (more than a full month) and 14.7% year over year. Weather played a role, but other factors are at work. Tariffs and threats of trade wars impact this region disproportionately given its central role in the nation’s industrial production.

— Backlog in the West surged to its highest level since mid-2014. Rebuilding from prior wildfires likely played a role, but the bigger reason relates to surging technology sectors in San Jose, Calif., San Francisco, Seattle, Portland, Ore., Los Angeles and San Diego.

Highlights by Industry

— Backlog in the commercial/institutional segment fell for the first time since the end of 2016. Despite the 8.8% quarterly decline, backlog in this segment remains 3.2% higher than the same time one year ago. However, this sector is vulnerable to further declines given its significant exposure to rising borrowing costs, higher materials prices and growing concerns regarding product saturation in a number of first-tier American real estate markets.

— Average backlog in the heavy industrial category rebounded during the first quarter, expanding 13.5%. Despite this sizable increase, the segment remains roughly unchanged at historically low levels on a year-over-year basis. Construction spending related to manufacturing has been drifting lower for months. While there have been some highly visible announcements regarding large capital projects in this segment, concerns regarding trade wars are likely to suppress backlog to a meaningful degree.

— Backlog in the infrastructure category drifted back to Earth during the first quarter, declining by more than two months from levels observed during the fourth quarter of 2017. This reading may have been impacted by a sharp increase in survey participation. Weather likely played an even larger role. The expectation is that backlog in this category will expand for the balance of the year as improving state and local government finances spur more investment in education, public safety, highway/street and other publicly financed categories.

Highlights by Company Size

— Large firms—those with annual revenues in excess of $100 million—experienced a sharp decline in backlog. This overlapped neatly with the decline in backlog related to infrastructure. Backlog for these large firms remains higher than any other classification considered in this release.

— Backlog among firms with annual revenues between $50 million and $100 million increased 0.4 months during the first quarter and currently stands at its second highest level since the series began in 2008. This group is heavily impacted by certain construction segments that have experienced little interruption in construction spending momentum.

— Firms with between $30 million and $50 million in annual revenues experienced a sharp decline in first quarter backlog. Enhanced survey participation likely explains part of this result. This group is significantly exposed to the energy sector, which stands to see an uptick in activity given recent trends in oil prices.

— Backlog for firms with annual revenues of less than $30 million increased 0.3 months during the first quarter and remains remarkable steady. This stability is likely the product of a dearth of available subcontractors to do electrical, mechanical, glass installation and other forms of work.

CBI is a leading economic indicator that reflects the amount of construction work under contract, but not yet completed. CBI is measured in months, with a lengthening backlog implying expanding demand for construction services. More CBI charts and graphs are available on abc.org.

Related Stories

Market Data | Oct 1, 2021

Nonresidential construction spending dips in August

Spending declined on a monthly basis in 10 of the 16 nonresidential subcategories.

Market Data | Sep 29, 2021

One-third of metro areas lost construction jobs between August 2020 and 2021

Lawrence-Methuen Town-Salem, Mass. and San Diego-Carlsbad, Calif. top lists of metros with year-over-year employment increases.

Market Data | Sep 28, 2021

Design-Build projects should continue to take bigger shares of construction spending pie over next five years

FMI’s new study finds collaboration and creativity are major reasons why owners and AEC firms prefer this delivery method.

Market Data | Sep 22, 2021

Architecture billings continue to increase

The ABI score for August was 55.6, up from July’s score of 54.6.

Market Data | Sep 20, 2021

August construction employment lags pre-pandemic peak in 39 states

The coronavirus delta variant and supply problems hold back recovery.

Market Data | Sep 15, 2021

ABC’s Construction Backlog Indicator plummets in August; Contractor Confidence down

ABC’s Construction Confidence Index readings for sales, profit margins and staffing levels all fell modestly in August.

Market Data | Sep 7, 2021

Construction sheds 3,000 jobs in August

Gains are limited to homebuilding as other contractors struggle to fill both craft and salaried positions.

Market Data | Sep 3, 2021

Construction workforce shortages reach pre-pandemic levels

Coronavirus continues to impact projects and disrupt supply chains.

Multifamily Housing | Sep 1, 2021

Top 10 outdoor amenities at multifamily housing developments for 2021

Fire pits, lounge areas, and covered parking are the most common outdoor amenities at multifamily housing developments, according to new research from Multifamily Design+Construction.

Market Data | Sep 1, 2021

Construction spending posts small increase in July

Coronavirus, soaring costs, and supply disruptions threaten to erase further gains.