Associated Builders and Contractors reported today that its Construction Backlog Indicator expanded to 8.9 months in May 2019, up 0.2 months or 2.2% since April 2019, when CBI stood at 8.7 months.

“Nonresidential construction spending continues to be a significant source of economic strength in America, and the latest Construction Backlog Indicator strongly suggests that nonresidential construction spending will continue to be a major driver of business revenue growth and employment,” said ABC Chief Economist Anirban Basu. “Despite concerns about the rising costs of material prices and labor impacting construction contracts, demand for nonresidential construction services remains elevated for now.

“In general, nonresidential construction spending patterns lag the broader economy by 12-18 months,” said Basu. “While nonresidential construction doesn’t keep pace with other industry segments during the early stages of an economic recovery, it can continue to see robust growth during the late stages of an economic expansion. With the economy continuing to demonstrate momentum along the dimensions of financial market performance, job creation, income growth and consumer spending, contractors can expect several additional quarters of spending growth.

“That said, infrastructure backlog declined sharply in May, which is likely a statistical aberration,” said Basu. “The infrastructure category is dominated by several very large firms, and changes in their idiosyncratic backlog can have major impacts on the overall reading. There is little reason to expect a meaningful dip in infrastructure spending in the near term given the improving financial health of many states and localities across the nation. Moreover, backlog in the commercial/institutional and heavy industrial segments rose in May. Several construction firms specializing in heavy industrial construction in the Midwest report substantial increases in construction backlog.”

Related Stories

Market Data | Oct 19, 2021

Demand for design services continues to increase

The Architecture Billings Index (ABI) score for September was 56.6.

Market Data | Oct 14, 2021

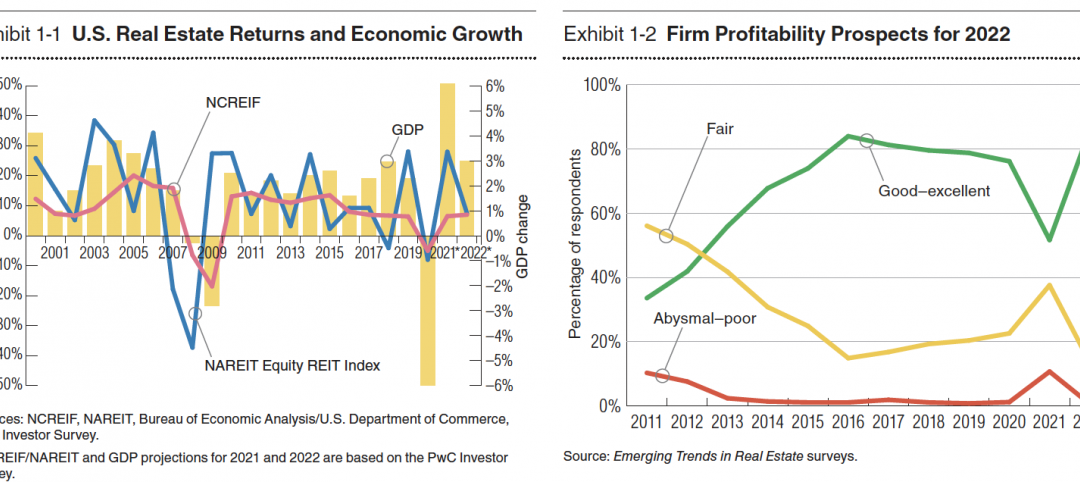

Climate-related risk could be a major headwind for real estate investment

A new trends report from PwC and ULI picks Nashville as the top metro for CRE prospects.

Market Data | Oct 14, 2021

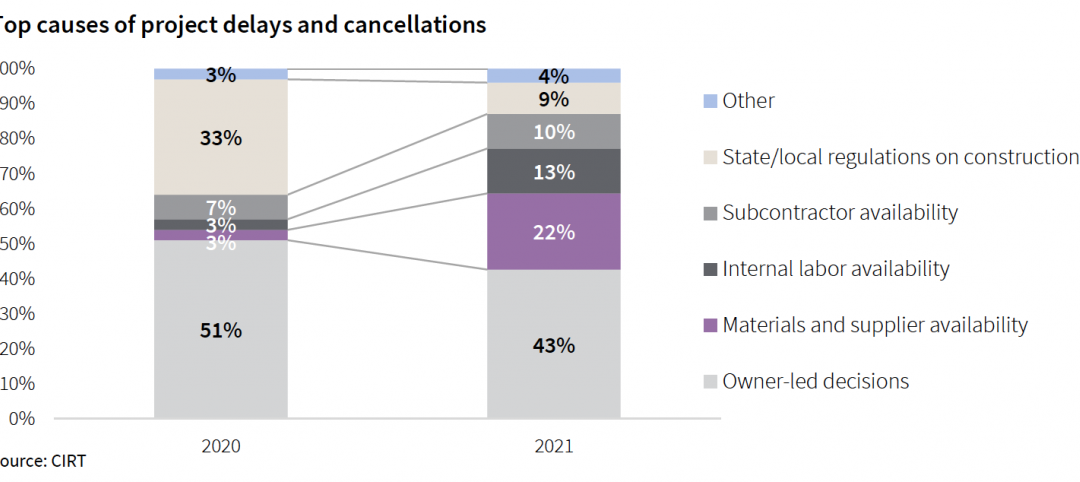

Prices for construction materials continue to outstrip bid prices over 12 months

Construction officials renew push for immediate removal of tariffs on key construction materials.

Market Data | Oct 11, 2021

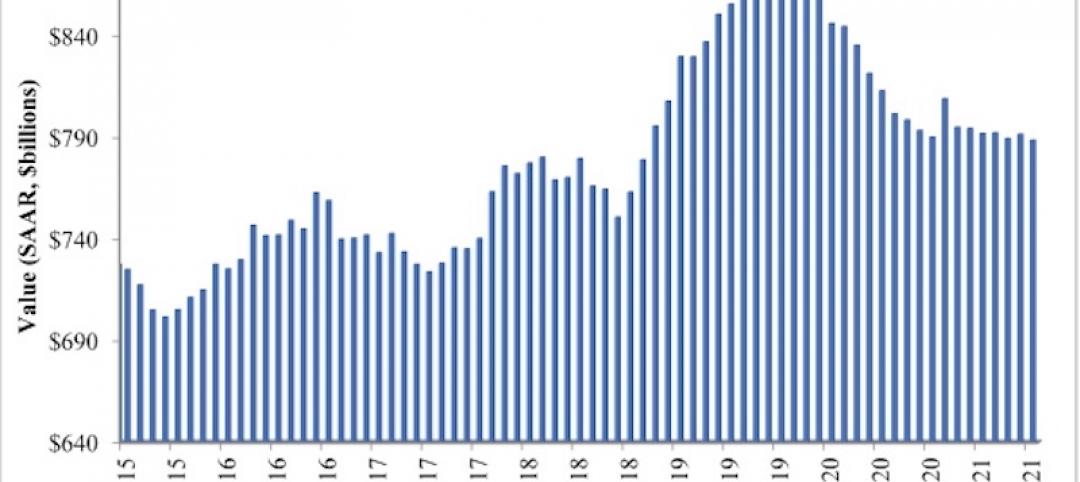

No decline in construction costs in sight

Construction cost gains are occurring at a time when nonresidential construction spending was down by 9.5 percent for the 12 months through July 2021.

Market Data | Oct 11, 2021

Nonresidential construction sector posts first job gain since March

Has yet to hit pre-pandemic levels amid supply chain disruptions and delays.

Market Data | Oct 4, 2021

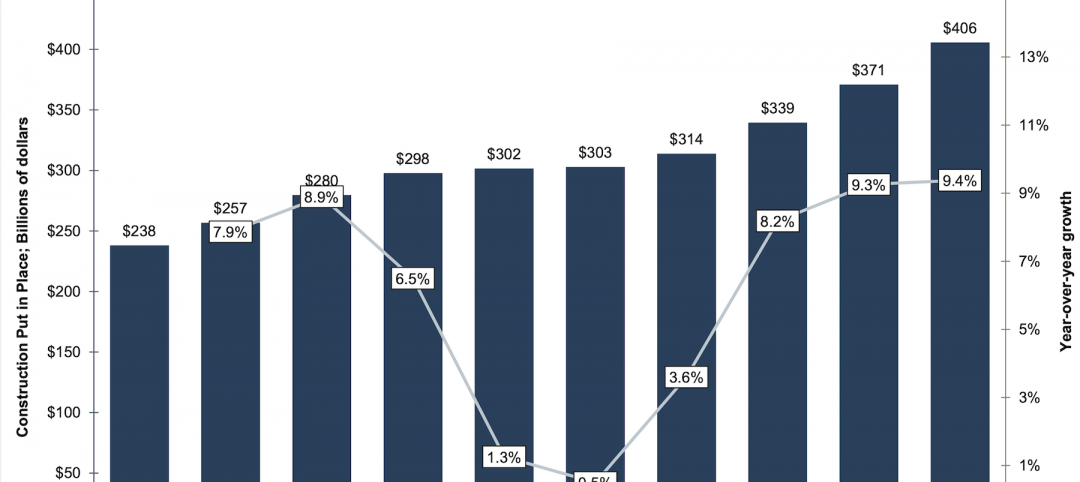

Construction spending stalls between July and August

A decrease in nonresidential projects negates ongoing growth in residential work.

Market Data | Oct 1, 2021

Nonresidential construction spending dips in August

Spending declined on a monthly basis in 10 of the 16 nonresidential subcategories.

Market Data | Sep 29, 2021

One-third of metro areas lost construction jobs between August 2020 and 2021

Lawrence-Methuen Town-Salem, Mass. and San Diego-Carlsbad, Calif. top lists of metros with year-over-year employment increases.

Market Data | Sep 28, 2021

Design-Build projects should continue to take bigger shares of construction spending pie over next five years

FMI’s new study finds collaboration and creativity are major reasons why owners and AEC firms prefer this delivery method.

Market Data | Sep 22, 2021

Architecture billings continue to increase

The ABI score for August was 55.6, up from July’s score of 54.6.