Associated Builders and Contractors reports today that its Construction Backlog Indicator rose to 8.0 months in May, according to an ABC member survey conducted from May 20 to June 2, 0.1 months higher than in April 2021 and May 2020.

While ABC’s Construction Confidence Index readings for sales increased modestly in May, confidence regarding profit margins and staffing levels slipped. All three indices remain above the threshold of 50, indicating expectations of growth over the next six months.

“Nonresidential construction backlog continues to edge higher, consistent with expectations that sales, profit margins and staffing will expand over the next six months,” said ABC chief economist Anirban Basu. “For at least four reasons, this represents an extraordinary set of findings.

“First, materials prices have risen significantly over the past year and labor costs are also on the rise,” said Basu. “All things equal, one might think this would suppress profit margin growth. Apparently, demand for construction services is strong enough to generate sufficient pricing power to more than fully countervail those factors. Second, skills shortages continue to impact the construction industry and many other segments. Despite that, the average nonresidential contractor expects to expand their teams during the months ahead.

“Third, conventional wisdom suggests that commercial real estate fundamentals are weak in the context of remote working, online shopping and sluggish business travel,” said Basu. “Nonetheless, backlog in the commercial category remains stable. Fourth and finally, while there has been much talk about a federal infrastructure plan, it remains elusive. Nonetheless, backlog in the infrastructure category rose significantly in May, perhaps a reflection of stronger state and local government balance sheets and associated increases in infrastructure outlays. In sum, contractors can expect healthy growth in activity through the balance of 2021.”

Related Stories

Market Data | Nov 22, 2021

Only 16 states and D.C. added construction jobs since the pandemic began

Texas, Wyoming have worst job losses since February 2020, while Utah, South Dakota add the most.

Market Data | Nov 10, 2021

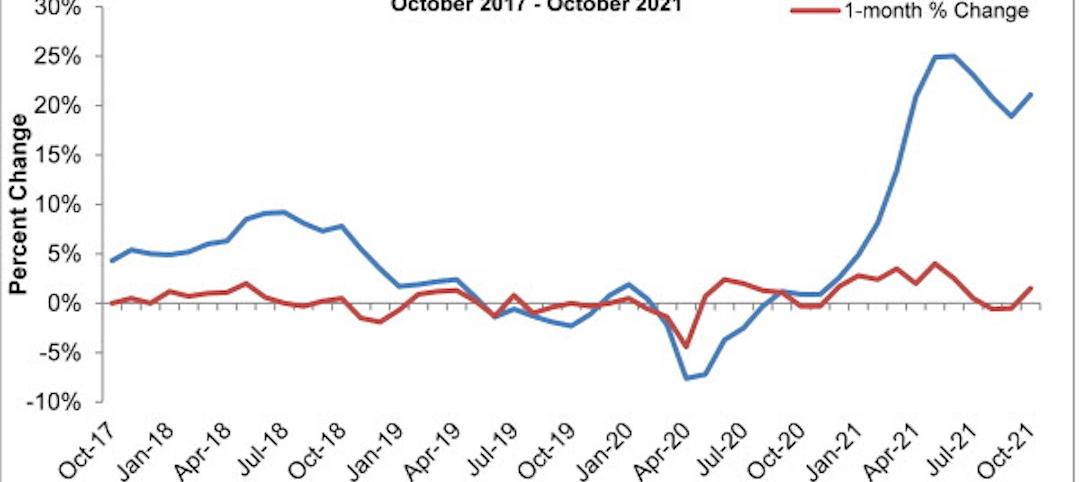

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

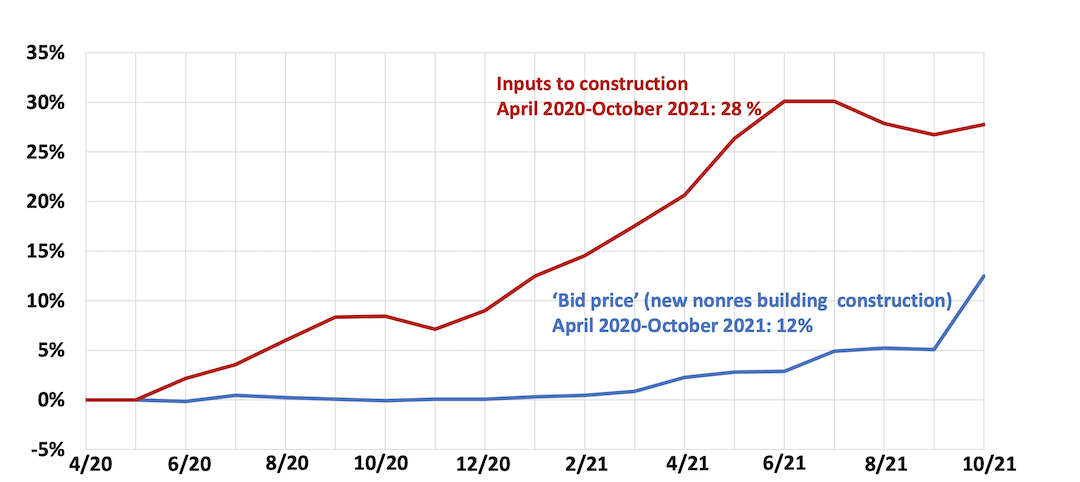

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.

Market Data | Oct 26, 2021

U.S. construction pipeline experiences highs and lows in the third quarter

Renovation and conversion pipeline activity remains steady at the end of Q3 ‘21, with conversion projects hitting a cyclical peak, and ending the quarter at 752 projects/79,024 rooms.