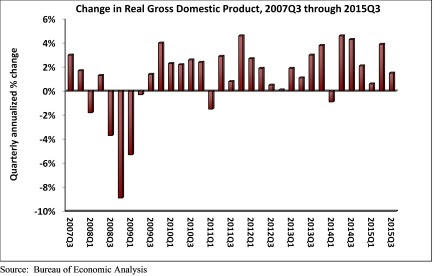

Both real gross domestic product (GDP) and nonresidential fixed investment expanded during the third quarter, according to an analysis by Associated Builders and Contractors (ABC) of a release from the Bureau of Economic Analysis. GDP expanded 1.5% (seasonally adjusted annual rate) during the third quarter while nonresidential fixed investment expanded by 2.1% during that period, both building on positive results from the previous quarter.

The bureau estimated that GDP expanded 3.9% during the year's second quarter, while nonresidential fixed investment was revised upward to a 4.1% increase from an initial estimate of a 0.6% decrease. This marks the second consecutive release in which the previous quarter's nonresidential fixed investment figure was amended from negative to positive. Investment in nonresidential structures fell by 4% after growing by 6.2% in the second quarter.

"The U.S. economy is not quite as bad as the headline GDP number suggests," said ABC Chief Economist Anirban Basu in a statement. "Private final demand, an indicator that represents sales to nongovernmental domestic purchasers, expanded by 3.2% in the third quarter. Many economists consider this the most telling and persistent aspect of GDP, suggesting that the economy is healthier than some might suspect.

"The current quarter was heavily impacted by a foreseeable inventory adjustment, a stronger dollar and a weakening global economy," Basu said. "The fact that the recovery remains in place is reflected in fixed investment data, including the categories that relate most directly to nonresidential construction. While it is true that investment in structures slipped 4%, this largely appears to be a statistical give-back from the second quarter's better than 6% performance. Other data indicates ongoing momentum in nonresidential construction, which should be more apparent during ensuing GDP releases.

"The recovery will continue to be led by consumers," Basu said. "Interest rates will also feature prominently in terms of determining the extent to which the recovery will be sustained in 2016 and beyond. For now, ultra-low interest rates are inducing people to invest in order to generate financial yields. This has been a bonus for nonresidential construction, but potentially may be triggering over investment in certain construction segments."

Performance of key segments during the third quarter:

- Personal consumption expenditures added 2.19% to GDP after contributing 2.42% in the second quarter.

- Spending on goods grew 4.5% from the second quarter.

- Real final sales of domestically produced output increased 2.9% for the third quarter after a 3.7% increase in the second quarter.

- Federal government spending increased 0.2% in the third quarter after remaining unchanged in the second quarter.

- Nondefense spending increased 2.8% after decreasing by 0.5% in the previous quarter.

- National defense spending fell 1.4% after inching 0.3% higher in the second quarter.

- National defense spending fell 1.5% after growing 1% in the first quarter.

- State and local government spending expanded 2.6% during the third quarter after an increase of 4.3% in the second.

To view the previous GDP report, click here.

Related Stories

| Jul 22, 2013

Competitive pressures push academia to improve residences, classrooms, rec centers [2013 Giants 300 Report]

College and university construction continues to suffer from strained government spending and stingy commercial credit.

| Jul 22, 2013

Top K-12 School Sector Construction Firms [2013 Giants 300 Report]

Gilbane, Balfour Beatty, Turner top Building Design+Construction's 2013 ranking of the largest K-12 school sector contractors and construction management firms in the U.S.

| Jul 22, 2013

Top K-12 School Sector Engineering Firms [2013 Giants 300 Report]

AECOM, URS, STV top Building Design+Construction's 2013 ranking of the largest K-12 school sector engineering and engineering/architecture firms in the U.S.

| Jul 22, 2013

Top K-12 School Sector Architecture Firms [2013 Giants 300 Report]

DLR, SHW top Building Design+Construction's 2013 ranking of the largest K-12 school sector architecture and architecture/engineering firms in the U.S.

| Jul 22, 2013

Top University Sector Construction Firms [2013 Giants 300 Report]

Whiting-Turner, Turner, Skanska top Building Design+Construction's 2013 ranking of the largest university sector contractors and construction management firms.

| Jul 22, 2013

Top University Sector Engineering Firms [2013 Giants 300 Report]

Affiliated Engineers, URS, AECOM top Building Design+Construction's 2013 ranking of the largest university sector engineering and engineering/architecture firms in the U.S.

| Jul 22, 2013

Top University Sector Architecture Firms [2013 Giants 300 Report]

Cannon, Perkins+Will, Stantec top Building Design+Construction's 2013 ranking of the largest university sector architecture and architecture/engineering firms in the U.S.

| Jul 22, 2013

Top Office Sector Construction Firms [2013 Giants 300 Report]

Turner, Structure Tone, PCL top Building Design+Construction's 2013 ranking of the largest office sector contractors and construction management firms in the U.S.

| Jul 22, 2013

Top Office Sector Engineering Firms [2013 Giants 300 Report]

AECOM, Parsons Brinckerhoff, Jacobs top Building Design+Construction's 2013 ranking of the largest office sector engineering and engineering/architecture firms in the U.S.

, Kendall/Heaton (AOR), Francis Cauffman (workplace consultant, interiors), Wick Fisher White (MEP/fire engineer, interiors), and Thornton Tomasetti (SE). PHOTO: JOHN GEORGE")

| Jul 22, 2013

Market gains encourage better workplace design [2013 Giants 300 Report]

The commercial office sector is finally heating up, led by corporate headquarter and medical office building projects.