Associated Builders and Contractors' (ABC) Construction Backlog Indicator (CBI) expanded by 1% to 8.5 months during the 2nd quarter of 2015. Backlog declined 3% during the 1st quarter, which was punctuated by harsh winter weather and the lingering effects of the West Coast ports slowdown. CBI stands roughly where it did a year ago, indicative of an ongoing recovery in the nation's nonresidential construction industry.

"The nation's nonresidential construction industry is now one of America's leading engines of growth," said ABC Chief Economist Anirban Basu. "The broader U.S. economic recovery is now in its 74th month, but remains under-diversified, led primarily by a combination of consumer spending growth as well as residential and nonresidential construction recovery. Were the overall economy in better shape, the performance of nonresidential construction would not be as closely watched. The economic recovery remains fragile despite a solid GDP growth figure for the second quarter, and must at some point negotiate an interest-rate tightening cycle. Recent stock market volatility has served to remind all stakeholders how delicate the economic recovery continues to be."

Regional Highlights

- The West experienced a significant expansion in backlog, rising 1.2 months following the resolution of the West Coast port slowdown, however backlog in the region remains nearly 2.5 months below its year-ago levels, the largest drop of any region.

- Backlog in the South has essentially returned to where it was two years ago, in part because of a slowdown in energy-related investment. The implication is that the average contractor remains busy, but boom-like conditions no longer prevail in energy-intensive communities.

- Despite this, backlog in the South continue to hold the longest average construction backlog.

- Backlog slipped for a second consecutive quarter in the Northeast, but remains above levels registered during the second half of 2013.

- See charts and graphs here.

Industry Highlights

- Backlog in the heavy industrial segment has never been higher during the length of the series, penetrating the seven-month mark for the first time. This represents an increase of more than two months in average backlog over the past two years. Average backlog was below five months during 2013's second half.

- Industrial backlog has continued to rise despite the strength of the U.S. dollar, which has contributed to limited export growth.

- Commercial/institutional backlog has remained above eight months on average for twelve consecutive quarters, a reflection of America's steady rate of employment expansion.

- Backlog for all industry segments is higher on a year-over-year basis with exception of the commercial/institutional segment. Commercial/institution construction segments have been among the most active from a construction spending perspective in recent years. Therefore, the small adjustment in average backlog is not particularly worrisome.

- See charts and graphs here.

Highlights by Company Size

- On a quarterly basis, backlog rose or remained flat across all firm sizes.

- Average construction backlog is higher or roughly the same as year-ago levels for firms of all size categories with the exception of a half-month drop in backlog among firms generating $100 million or more in annual revenues.

- The largest firms, however, continue to have the lengthiest average backlog at 10.7 months.

- See charts and graphs here.

Related Stories

Contractors | Aug 4, 2017

4 ways to prepare for a negotiation

Practice, practice, practice, and understanding both sides of the deliberation are critical to success in any negotiation.

Laboratories | Aug 3, 2017

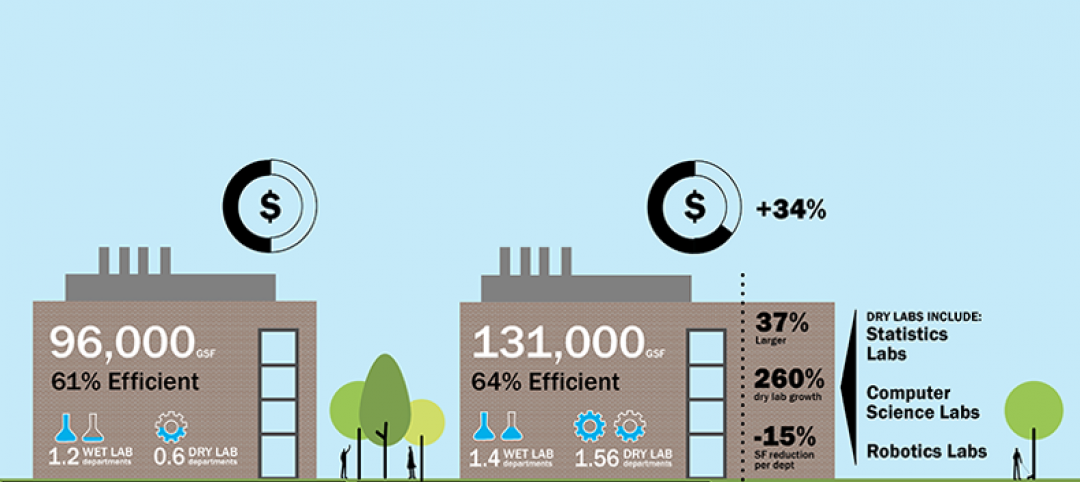

Today’s university lab building by the numbers

A three-month study of science facilities conducted by Shepley Bulfinch reveals key findings related to space allocation, size, and cost.

Lighting | Aug 2, 2017

Dynamic white lighting mimics daylighting

By varying an LED luminaire’s color temperature, it is possible to mimic daylighting, to some extent, and the natural circadian rhythms that accompany it, writes DLR Group’s Sean Avery.

Healthcare Facilities | Aug 2, 2017

8 healthcare design lessons from shadowing a nurse

From the surprising number of “hunting and gathering” trips to the need for quiet spaces for phone calls, interior designer Carolyn Fleetwood Blake shares her takeaways from a day shadowing a nurse.

High-rise Construction | Aug 1, 2017

Construction on the world’s skinniest tower halts due to ballooning costs

The planned 82-story tower has stalled after completing just 20 stories.

Multifamily Housing | Jul 27, 2017

Apartment market index: Business conditions soften, but still solid

Despite some softness at the high end of the apartment market, demand for apartments will continue to be substantial for years to come, according to the National Multifamily Housing Council.

Multifamily Housing | Jul 27, 2017

Game rooms and game simulators popular amenities in multifamily developments

The number of developments providing space for physical therapy was somewhat surprising, according to a new survey.

Building Enclosure Systems | Jul 26, 2017

Balcony and roof railings and the code: Maintain, repair, or replace? [AIA course]

Lacking familiarity with current requirements, some owners or managers complete a roof or balcony rehabilitation, only to learn after the fact that they need to tear noncompliant railings out of their new roof or terrace and install new ones.

Concrete | Jul 13, 2017

LF Driscoll and Balfour Beatty recently wrapped the largest concrete pour in Philadelphia’s history

The pour created the foundation for the Foster + Partners-designed Pavilion on Penn Medicine’s Campus.

Multifamily Housing | Jul 12, 2017

Midyear Rent Report: 26 states saw rental price increases in first half of 2017

The most notable rental increases are in growing markets in the South and Southwest: New Orleans, Glendale, Ariz., Houston, Reno, N.V., and Atlanta.