According to a new report from the American Institute of Architects, the nonresidential building sector is expected to see a healthy rebound through next year after failing to recover with the broader economy last year.

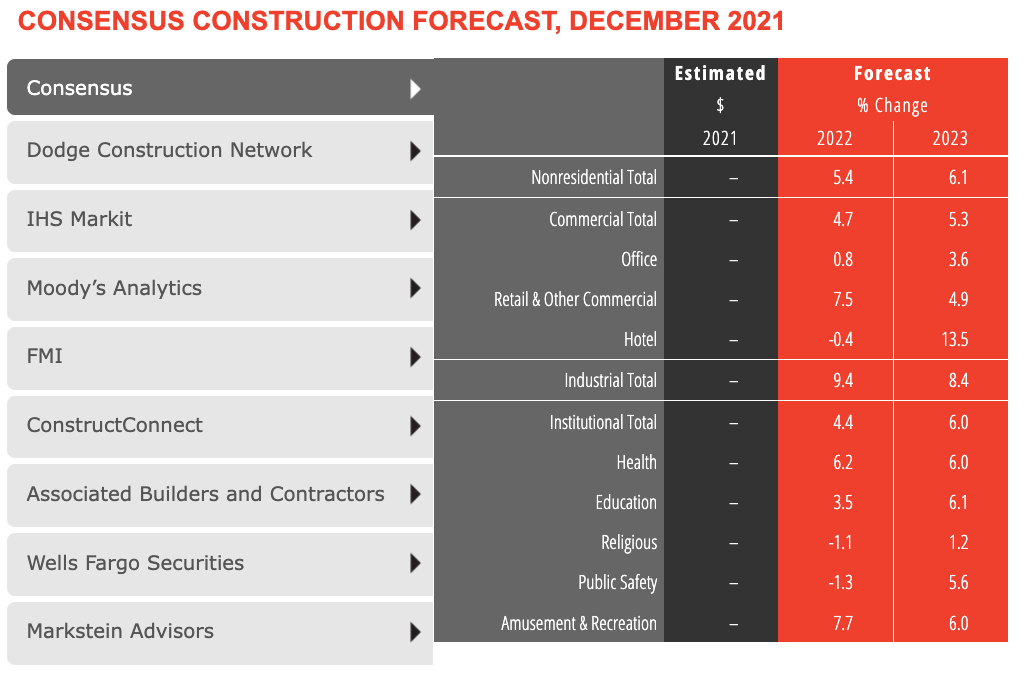

The AIA’s Consensus Construction Forecast panel—comprising leading economic forecasters—expects spending on nonresidential building construction to increase by 5.4 percent in 2022, and accelerate to an additional 6.1 percent increase in 2023. With a five percent decline in construction spending on buildings last year, only retail and other commercial, industrial, and health care facilities managed spending increases.

This year, only the hotel, religious, and public safety sectors are expected to continue to decline. By 2023, all the major commercial, industrial, and institutional categories are projected to see at least reasonably healthy gains.

“The pandemic, supply chain disruptions, growing inflation, labor shortages, and the potential passage of all or part of the Build Back Better legislation could have a dramatic impact on the construction sector this year,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “Challenges to the economy and the construction industry notwithstanding, the outlook for the nonresidential building market looks promising for this year and next.”

CLICK HERE TO VIEW INTERACTIVE CHART

More from AIA:

- The recovery in the broader economy in 2021 didn’t carry over to the nonresidential building sector. Spending on the construction of these facilities declined about 5%, on top of the 2% decline in 2020.

- The broader economy has seen a solid recovery since the depths of the pandemic-induced recession. It grew by about 5% last year and now has fully recovered from the past recession. There were almost 4 million net new payroll positions added last year, bringing national employment almost back to the level it was at in February 2020 prior to the pandemic. The national unemployment rate was 3.9% at the end of last year, just above the 3.5% rate in February 2020.

- In spite of these positive economic indicators, there are several headwinds to future economic growth. The uncertainty surrounding combatting Covid and its variants have added tremendous uncertainty to future building needs. The Biden Administration’s Build Back Better program was slated to add significant support to the construction sector, but its funding is very much in doubt at present (January 2022). Supply chain disruptions are likely to continue slow economic growth well into this year. Inflation accelerated during the second half of last year to its highest rate in almost four decades, which is expected to put upward pressure on interest rates. Finally, the already-serious labor shortages look to become even more severe this year and next.

- Industries throughout the economy are finding it challenging to retain their current employees and are having difficulty recruiting new ones. Most workers feel that jobs are plentiful, and therefore are increasingly comfortable leaving their current job in favor of searching for a better one. A recent survey of architecture firm leaders found that more than four in ten feel that recruiting architectural staff is a serious problem at present, and that it may create difficulties for the firm over the coming months given anticipated project workloads.

Related Stories

| Aug 11, 2010

Construction employment shrinks in 319 of the nation's 336 largest metro areas in July, continuing months-long slide

Construction workers in communities across the country continued to suffer extreme job losses this July according to a new analysis of metropolitan area employment data from the Bureau of Labor Statistics released today by the Associated General Contractors of America. That analysis found construction employment declined in 319 of the nation’s largest communities while only 11 areas saw increases and six saw no change in construction employment between July 2008 and July 2009.

| Aug 11, 2010

Green consultant guarantees LEED certification or your money back

With cities mandating LEED (Leadership in Energy and Environmental Design) certification for public, and even private, buildings in growing numbers, an Atlanta-based sustainability consulting firm is hoping to ease anxieties over meeting those goals with the industry’s first Green Guaranteed.

| Aug 11, 2010

Skanska, Turner most active in U.S. hotel construction, according to BD+C's Giants 300 report

A ranking of the Top 50 Hotel Contractors based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit http://www.BDCnetwork.com/Giants

| Aug 11, 2010

Gilbane, Whiting-Turner among nation's largest university contractors, according to BD+C's Giants 300 report

A ranking of the Top 50 University Contractors based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit /giants

| Aug 11, 2010

Suffolk breaks ground on colorful charter school in Boston

Suffolk Education has broken ground and began renovations and construction of a new $39.6 million facility to house the Boston Renaissance Charter Public School. The Suffolk team is renovating an existing, three-story mill building and warehouse in the Hyde Park section of Boston, Massachusetts, and constructing a 20,000 square-foot addition.

| Aug 11, 2010

McCarthy, Skanska among nation's largest healthcare contractors, according to BD+C's Giants 300 report

A ranking of the Top 50 Healthcare Contractors based on Building Design+Construction's 2009 Giants 300 survey. For more Giants 300 rankings, visit http://www.BDCnetwork.com/Giants

| Aug 11, 2010

Turner, Webcor, Hensel Phelps top BD+C's list of the 75 largest green contractors

With more than $3 billion in value of construction put in place for green buildings in 2008, Turner Construction tops BD+C’s ranking of the nation’s 75 largest green contractors, published as part of the Giants 300 report. Webcor Builders ($2.27 billion), Hensel Phelps Construction ($2.10 billion), The Whiting-Turner Contracting Co. ($1.97 billion), and Clark Group ($1.89 billion) round out the top five.