According to a new report from the American Institute of Architects, the nonresidential building sector is expected to see a healthy rebound through next year after failing to recover with the broader economy last year.

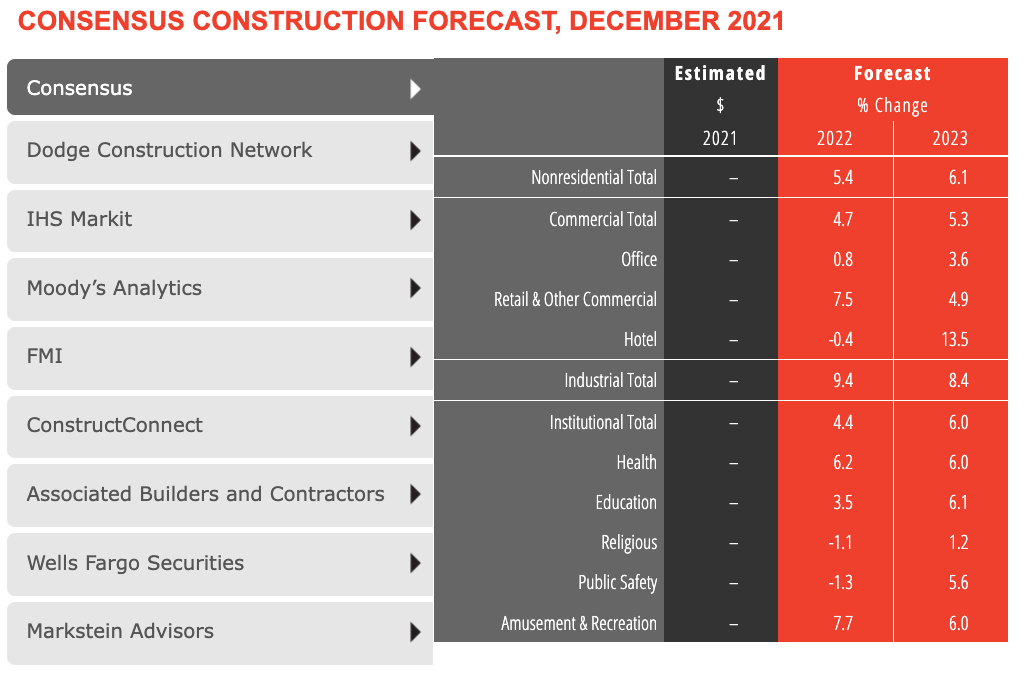

The AIA’s Consensus Construction Forecast panel—comprising leading economic forecasters—expects spending on nonresidential building construction to increase by 5.4 percent in 2022, and accelerate to an additional 6.1 percent increase in 2023. With a five percent decline in construction spending on buildings last year, only retail and other commercial, industrial, and health care facilities managed spending increases.

This year, only the hotel, religious, and public safety sectors are expected to continue to decline. By 2023, all the major commercial, industrial, and institutional categories are projected to see at least reasonably healthy gains.

“The pandemic, supply chain disruptions, growing inflation, labor shortages, and the potential passage of all or part of the Build Back Better legislation could have a dramatic impact on the construction sector this year,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “Challenges to the economy and the construction industry notwithstanding, the outlook for the nonresidential building market looks promising for this year and next.”

CLICK HERE TO VIEW INTERACTIVE CHART

More from AIA:

- The recovery in the broader economy in 2021 didn’t carry over to the nonresidential building sector. Spending on the construction of these facilities declined about 5%, on top of the 2% decline in 2020.

- The broader economy has seen a solid recovery since the depths of the pandemic-induced recession. It grew by about 5% last year and now has fully recovered from the past recession. There were almost 4 million net new payroll positions added last year, bringing national employment almost back to the level it was at in February 2020 prior to the pandemic. The national unemployment rate was 3.9% at the end of last year, just above the 3.5% rate in February 2020.

- In spite of these positive economic indicators, there are several headwinds to future economic growth. The uncertainty surrounding combatting Covid and its variants have added tremendous uncertainty to future building needs. The Biden Administration’s Build Back Better program was slated to add significant support to the construction sector, but its funding is very much in doubt at present (January 2022). Supply chain disruptions are likely to continue slow economic growth well into this year. Inflation accelerated during the second half of last year to its highest rate in almost four decades, which is expected to put upward pressure on interest rates. Finally, the already-serious labor shortages look to become even more severe this year and next.

- Industries throughout the economy are finding it challenging to retain their current employees and are having difficulty recruiting new ones. Most workers feel that jobs are plentiful, and therefore are increasingly comfortable leaving their current job in favor of searching for a better one. A recent survey of architecture firm leaders found that more than four in ten feel that recruiting architectural staff is a serious problem at present, and that it may create difficulties for the firm over the coming months given anticipated project workloads.

Related Stories

Market Data | Jan 7, 2021

Few construction firms will add workers in 2021 as industry struggles with declining demand, growing number of project delays and cancellations

New industry outlook finds most contractors expect demand for many categories of construction to decline.

Market Data | Jan 5, 2021

Barely one-third of metros add construction jobs in latest 12 months

Dwindling list of project starts forces contractors to lay off workers.

Market Data | Jan 4, 2021

Nonresidential construction spending shrinks further in November

Many commercial projects languish, even while homebuilding soars.

Market Data | Dec 29, 2020

Multifamily transactions drop sharply in 2020, according to special report from Yardi Matrix

Sales completions at end of Q3 were down over 41 percent from the same period a year ago.

Market Data | Dec 28, 2020

New coronavirus recovery measure will provide some needed relief for contractors coping with project cancellations, falling demand

Measure’s modest amount of funding for infrastructure projects and clarification that PPP loans may not be taxed will help offset some of the challenges facing the construction industry.

Market Data | Dec 28, 2020

Construction employment trails pre-pandemic levels in 35 states despite gains in industry jobs from October to November in 31 states

New York and Vermont record worst February-November losses, Virginia has largest pickup.

Market Data | Dec 16, 2020

Architecture billings lose ground in November

The pace of decline during November accelerated from October, posting an Architecture Billings Index (ABI) score of 46.3 from 47.5.

AEC Tech | Dec 8, 2020

COVID-19 affects the industry’s adoption of ConTech in different ways

A new JLL report assesses which tech options got a pandemic “boost.”

Market Data | Dec 7, 2020

Construction sector adds 27,000 jobs in November

Project cancellations, looming PPP tax bill will undercut future job gains.

Market Data | Dec 3, 2020

Only 30% of metro areas add construction jobs in latest 12 months

Widespread project postponements and cancellations force layoffs.